The Teranet January 2011 data have been released.

If you want to see the composite, which is running flat, you have to look in the lower right under the heading "Historical Charts - National Composite" and click on "Index Values and Sales Pair Count".

Vancouver rising.

Calgary down 1% month on month, which is an acceleration from the last two months. Another observation about Calgary is how sharp the discontinuity is in 2006. Might have something to do with the Spot Price of Brent Crude.

Toronto rising, just slightly. 1/2% gain month on month.

Ottawa on a steady decline that began in November 2010 and still rolls on at 1/2% per month.

Montreal rising slightly. Note that Montreal is the second most overpriced city in Canada. Unlike the others it shows much less of a dip during the 2008-2009 downturn.

Halifax up slightly, but the data are very noisy. I'm going to call it overall flat.

Wednesday, March 30, 2011

{kind=link}

Some Tidbits from the Downturn Downunder

First time homebuyers are getting scarce. Fundamentals outweigh even master spruiking.

Values dip as first home buyers lost

Money Morning Australia passes on comments (? if it's a report, I haven't found it) from an RE industry guy in a state of capitulation.

Real Estate Industry Forecasts Major Price Falls

Values dip as first home buyers lost

Around $220 billion is loaned to residential buyers across Australia each year, of which 15 per cent has been taken up by the first home buyer segment over the past decade, equating to about $30 billion per year.

But during the recent boost (2009), this rose to 24 per cent with the annual borrow close to $53 billion.

During 2009, there were 190,850 first home buyers across Australia but in 2010, this figure dropped dramatically to 96,200. Hence, we are now experiencing a market impacted by the absence of first home buyers.

Money Morning Australia passes on comments (? if it's a report, I haven't found it) from an RE industry guy in a state of capitulation.

Real Estate Industry Forecasts Major Price Falls

“We anticipate a reduction in the median price from $601,500 in December last year to somewhere between 3-5% below that in March.” – Enzo Raimondo, CEO, Real Estate Institute of Victoria.

It seems it’s not just the so-called lunatic fringe saying the housing bubble has burst.

. . .

Make no mistake, a 3-5% drop in the median house price is big. Especially if you’re mortgaged to the eyeballs. For some, when you take into account the fees associated with buying and selling, it can mean the difference between walking away break-even or walking away with a big loss.

And I mean big.

A 5% drop from $601,500 is a fall of $30,075.

Chinese Enforcement of House Price Limits, Round 1

China penalizes property developer for pushing up housing prices

"The next stage of our housing project will be available in the first half of 2011 at the earliest, and prices are very likely to exceed 8,000 yuan a square meter," the company said in a notice to potential home buyers last December.

Ganzhou's price bureau imposed a fine of 500,000 yuan on the company and ordered the repayment of all money collected from potential buyers, in accordance with the country's Price Law.

Tuesday, March 29, 2011

#8 in Signs That the End is Nigh

I'll figure out what 1-7 are later. This just feels like number eight.

The U.S. bust was marked by blame. Not blaming Greenspan for the cheap money. Not blaming cuts to regulation that let the banks and wall street print money (in essence) and flood the housing (and auto and boat and rv) markets with liquidity and wholly unregulated securitization that created a pull system that encouraged every player in the game to push loans onto anyone and everyone despite their inability to actually afford the payments. NO, the blame went to the bloggers who were pointing out that the market was overdue to turn. These bastions of personal opinion read by dozens (maybe even more!) of people were, of course, responsible for swaying the entire market. Their pithy words of warning caused real investors to ignore the fundamentals of a "sound market" and caused legions of house-hungry newlyweds to instead live with mom and dad.

Of course they had such far reaching impact from their little blogs. Especially when, as the bloggers were forced to point out, they had been making those warning for years to absolutely no effect. All of a sudden, it was all their fault.

Admittedly, blogs are far more mainstream than they were in the heady days of 2006, but I call corner on sign #8 for Australia.

Property market slump? Blame me

Newsflash: if market fundamentals are sound, no one (especially not investors looking for properties with positive cash flow) will pay one lick of attention. It's a threat now because . . . ?

The U.S. bust was marked by blame. Not blaming Greenspan for the cheap money. Not blaming cuts to regulation that let the banks and wall street print money (in essence) and flood the housing (and auto and boat and rv) markets with liquidity and wholly unregulated securitization that created a pull system that encouraged every player in the game to push loans onto anyone and everyone despite their inability to actually afford the payments. NO, the blame went to the bloggers who were pointing out that the market was overdue to turn. These bastions of personal opinion read by dozens (maybe even more!) of people were, of course, responsible for swaying the entire market. Their pithy words of warning caused real investors to ignore the fundamentals of a "sound market" and caused legions of house-hungry newlyweds to instead live with mom and dad.

Of course they had such far reaching impact from their little blogs. Especially when, as the bloggers were forced to point out, they had been making those warning for years to absolutely no effect. All of a sudden, it was all their fault.

Admittedly, blogs are far more mainstream than they were in the heady days of 2006, but I call corner on sign #8 for Australia.

Property market slump? Blame me

So, the phone rings…

Agent: I just wanted to find out if you’re going to be as negative this week as you have in the last four weeks about the market because you are single-handedly making my life very f**king hard by reporting doom and gloom.

Me: I get the numbers like everyone else and the numbers compared to other years aren’t particularly good.

Agent: I’ve got to say you’re in a very powerful position there and the readers believe everything they read. If it’s in print they believe it. Just try and be a bit more balanced in your views.

Me: If you can give me an instance when I haven’t been balanced…

Newsflash: if market fundamentals are sound, no one (especially not investors looking for properties with positive cash flow) will pay one lick of attention. It's a threat now because . . . ?

Mortgage Insurance Risks to the Canadian Taxpayer

CMHC is backed by the full credit of the Canadian taxpayer, but they are only 70% of the market.

What of the remaining 30% of the mortgage insurance market?

Rating Mortgage Insurance Companies in Canada

The tax payers are backing the vast bulk of all insured mortgages. One has to hope that the insurance companies are aggressive at put-backs. Moral hazard would suggest the banks are not being very careful with the mortgages they are issuing. Unfortunately, the precedent from the 2008 downturn is to turn CMHC into a bailout mechanism, rather than an instrument of fairness.

And it's not just high loan to value mortgages that are backed, it's also any mortgage that is destined for securitization.

From Inside CMHC from Canadian Mortgage Trends.com

I love in this interview how they say, oh well, all is good since we hold 2x the capital required by OSFI, but never actually say what that number is.

The Minimum Capital Test is here. Pages 35-41

Mortgage insurance margins range from $.10 to $1.10 on $100 of original mortgage amount with factors applied to these of .04 to 1.75. This supports the generally cited number of 1.5% or so. Minimum capital requirements vary by the portfolio the company is holding at any time.

Note: profits from CMHC all these years have been dividended back to the Canadian Government, i.e. the tax payers (except for 2008 when they held it back and built reserves instead). It's not like the potential capital they could have been holding vanished; it's been spent on other things. It's possible that if the mortgage insurance fee has been set properly, even if the capital requirements look thin, the tax payers will not end up in the red, overall, but they are acting as secondary insurers, whether they want to be or not. And in reality, mortgage insurance is just a tax since much of it goes on a pass thru to the government.

What of the remaining 30% of the mortgage insurance market?

Rating Mortgage Insurance Companies in Canada

• The insurance company covers 100% of the loan plus accrued interest against loss by the lender if the

borrower defaults.

• To establish a degree of parity between the CMHC and private MI providers, the government of Canada

provides a 90% guarantee of private MI claims. This places the private and public sector mortgage insurers

on a more level playing field for the purposes of calculating a lender’s risk exposure to MI providers.

The tax payers are backing the vast bulk of all insured mortgages. One has to hope that the insurance companies are aggressive at put-backs. Moral hazard would suggest the banks are not being very careful with the mortgages they are issuing. Unfortunately, the precedent from the 2008 downturn is to turn CMHC into a bailout mechanism, rather than an instrument of fairness.

And it's not just high loan to value mortgages that are backed, it's also any mortgage that is destined for securitization.

From Inside CMHC from Canadian Mortgage Trends.com

Pierre: At the end of 2008, the percentage of insured mortgages outstanding, compared to residential mortgage credit outstanding, was estimated at 68%.Unfortunately, I couldn't find any newer numbers than this.

Noteworthy: A large percentage of insured mortgages are under 80% loan-to-value. That’s because many lenders use CMHC “portfolio insurance” (which provides the same default insurance coverage as for high ratio mortgages) to lower capital requirements and/or as a prerequisite to securitizing their mortgages

I love in this interview how they say, oh well, all is good since we hold 2x the capital required by OSFI, but never actually say what that number is.

The Minimum Capital Test is here. Pages 35-41

Mortgage insurance margins range from $.10 to $1.10 on $100 of original mortgage amount with factors applied to these of .04 to 1.75. This supports the generally cited number of 1.5% or so. Minimum capital requirements vary by the portfolio the company is holding at any time.

Note: profits from CMHC all these years have been dividended back to the Canadian Government, i.e. the tax payers (except for 2008 when they held it back and built reserves instead). It's not like the potential capital they could have been holding vanished; it's been spent on other things. It's possible that if the mortgage insurance fee has been set properly, even if the capital requirements look thin, the tax payers will not end up in the red, overall, but they are acting as secondary insurers, whether they want to be or not. And in reality, mortgage insurance is just a tax since much of it goes on a pass thru to the government.

China Bubble Continues to Spread

Third tier cities now involved.

Evergrande's Net Soars on Tertiary Cities

Just in case you think these companies found some way to make money building affordable housing . . .

Evergrande's Net Soars on Tertiary Cities

"Given that third-tier cities are generally less affected by the macro adjustment and control policies, the room for urban development is broad and the demand and growth potential for housing are immense," said Chairman Hui Ka-yan.

As of Dec. 31, the group had total land reserves of about 96 million square meters distributed among 62 cities in China, including 21 second-tier cities and 39 third-tier cities.

Just in case you think these companies found some way to make money building affordable housing . . .

Evergrande said it will continue to pursue a development model focused on quickly bringing mid- and high-end housing to market, adding the company put more than 70% of its new development projects up for sale within six months of acquiring the land last year.

Friday, March 25, 2011

China Affordable Housing Expected Shortfall on Money and Profit

The lack of affordable housing doesn't affect the bubble, except as a foil to claim there is demand, but it does affect social stability, which could burst the bubble.

China’s Housing Plan to Face Financing Challenge, Cushman Says

China’s Housing Plan to Face Financing Challenge, Cushman Says

China’s biggest challenge in its plan to build 36 million affordable homes over five years is the ability to tap funding and draw developers to work on the projects, Cushman & Wakefield Inc. said.

The nation needs 1.3 trillion yuan ($198 billion) for its affordable homes this year, excluding land costs, Housing and Urban-Rural Development Vice Minister Qi Ji said on March 9. The central and local governments will only provide 500 billion yuan, Qi said.

Thursday, March 24, 2011

CHMC, Fannie Freddie, Baby Meet Bathwater

The CMHC: Canada’s mortgage monster

What is also roundly ignored is the role the Fannie and Freddie (and FHA) played after the crash, when every credit market was frozen, in providing a lender of last resort. People thought house prices fell rapidly as it was? Imagine no mortgages for months on end, at all. That is their true charter. We can get rid of Fannie and Freddie (and continue to ignore the real causes of the boom and bust), but without systemic repairs to the system that no one has the political will to make we are going to repeat this housing bubble, and be forced to recreate a Fannie/Freddie style entity to stave off another Great Depression when the markets again seize up. Be nice to actually address the real problems.

These types of entities can safely exist (Fannie and Freddie existed since 1938 and things went along fine until the deregulation of 1999/2000 that banned all oversight of derivatives), but their charter and their compensation need to be set down properly. Fannie and Freddie (and the 24/25 of the top mortgage lenders that didn't have to meet CRA, yet loaned out money to unqualified people) were allowed to operate in this reckless manner because the right people were getting rich off of it. Follow the money before following the politics. It's more likely to lead you to the root cause of the problem, and shed light on the solution, i.e., make management pay, personally, for losing other people's money.

CMHC is no different. The politics of housing for all is a convenient smokescreen. Who's making the money?

“Did the banks all of a sudden open up the lending spigots? In fact banks have actually reduced the number of their mortgages held from the peak of third quarter of 2008. The smoking gun is the CMHC and its securitization policies.”Moral Hazard, it isn't just for Wall Street.

Almost immediately, LePoidevin’s bosses at National Bank leapt to the CMHC’s defence.Ah, Cassandra, poor Cassandra.

Even worse, the public knows next to nothing about what lurks inside the CMHC’s books, aside from the smattering of details it releases in its annual report. And, unlike every other major insurance provider in the country, the CMHC doesn’t answer to Canada’s top financial services regulator.Really? That's weird and/or convenient. In the U.S. they had to answer, but the oversight agencies had been defunded to the point of uselessness. A process that is repeating itself forthwith given the Republican takeover of congress. Absent direct oversight the only hope is the incentive structure has been set up rationally.

Yet on specific decisions that dramatically loosened mortgage lending rules last decade, CMHC officials have testified they did so on their own with the approval and oversight of the CMHC’s board of directors—a board that includes a political consultant, real estate developers, a small-town lawyer and even the owner of a plumbing company—though not one single economist or recognizable financial services professional.Oh. Snap.

“The CMHC is influenced by the political process, just like [Fannie Mae and Freddie Mac] were in the United States,”They were influenced by profit more, specifically bonuses to management. If you want an entity like this to act in the best interests of others, the compensation needs to be designed to mimic the larger risks and rewards. Moral Hazard was operating at many levels. And if you interview these guys from Countrywide, BoA, etc, they still claim they don't know what happened. They never watched the numbers that mattered because from their perspective of making money for their pocket, they truly didn't matter.

What is also roundly ignored is the role the Fannie and Freddie (and FHA) played after the crash, when every credit market was frozen, in providing a lender of last resort. People thought house prices fell rapidly as it was? Imagine no mortgages for months on end, at all. That is their true charter. We can get rid of Fannie and Freddie (and continue to ignore the real causes of the boom and bust), but without systemic repairs to the system that no one has the political will to make we are going to repeat this housing bubble, and be forced to recreate a Fannie/Freddie style entity to stave off another Great Depression when the markets again seize up. Be nice to actually address the real problems.

These types of entities can safely exist (Fannie and Freddie existed since 1938 and things went along fine until the deregulation of 1999/2000 that banned all oversight of derivatives), but their charter and their compensation need to be set down properly. Fannie and Freddie (and the 24/25 of the top mortgage lenders that didn't have to meet CRA, yet loaned out money to unqualified people) were allowed to operate in this reckless manner because the right people were getting rich off of it. Follow the money before following the politics. It's more likely to lead you to the root cause of the problem, and shed light on the solution, i.e., make management pay, personally, for losing other people's money.

CMHC is no different. The politics of housing for all is a convenient smokescreen. Who's making the money?

It points out that the Canadian mortgage system is fundamentally different than in the U.S. . . . lenders can generally go after homeowners who don’t make their payments.I love this one. In a collapse there is no money to go after. This is no different than asserting that household balance sheets look healthy because you are including an inflated house value on the asset side.

says Serré, adding that rising home prices have also helped improve the debt picture.Oh, there it is. What do I win?

Serré declined to comment directly on Macdonell’s remarks. “I’m not exactly sure what low or poor credit is,” he says. “But I want to make clear that our mandate is not to get people into home ownership, our mandate is to provide the housing of choice. The last thing we want, as a government insurer, is to get people in a position where they can’t manage their debt.”What is "housing of choice"?

From the About Us page: Today, CMHC remains committed to helping Canadians access a wide choice of safe, quality, affordable homes, and making vibrant and sustainable communities and cities a reality across the countryRecent experience strongly suggests that, absent a equivalent-rent-adjusted limit on mortgage amounts, making mortgages more affordable simply makes housing unaffordable. Maybe you need to look at that charter again.

China Housing Price Controls Set Higher Than Analysts Expected

China’s Property Stocks Rally on Price Target Speculation (1)

Leaving aside the notion of enforcement of this law, if I'm reading this right, the rise year on year since December in places like Shanghai would be perfectly acceptable.

I do so want to see how they are going to try to implement this.

“There’s market speculation that local governments will set a target of limiting housing price gains to between zero percent and the GDP growth rate,” said Wang Weijun, a strategist at Zheshang Securities Co. in Shanghai. “That’s much better than the target of below zero percent anticipated by the market.” Local governments may announce their price control targets next week, Wang said.

Leaving aside the notion of enforcement of this law, if I'm reading this right, the rise year on year since December in places like Shanghai would be perfectly acceptable.

I do so want to see how they are going to try to implement this.

Tuesday, March 22, 2011

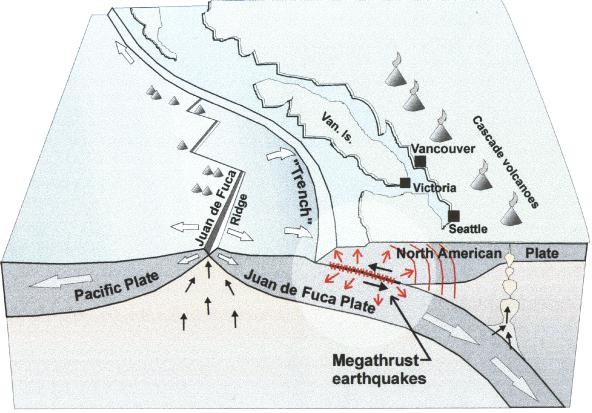

Earthquakes and Vancouver Housing Sentiment

Real estate, especially where prices have already exceeded the economic value of the underlying property (compared to rents), is susceptible to shifts in sentiment. Will the recent earthquakes on the other parts of the ring of fire cause buyers, specifically foreign buyers, to shy away? Vancouver is attractive as a haven, for money, from political uncertainty. One might expect that its lacking in being a long-term haven from natural disaster would damage that overall reputation. Not that anything in Vancouver or BC has changed, just that buyers' risk assessment will have.

I wondered how the real estate friendly press was handling this.

The Sun took the survey route, pointing out that residents don't believe their municipalities are prepared. This doesn't mean they aren't, just that people don't have faith.

The Times Colonist in Victoria takes a pablum approach. I especially like the close: She suggests the public visit the Provincial Emergency Program website at pep.bc.ca, or go to the "public health" section of www.viha.ca should an event occur. If it's a significant event, I'm not sure that's going to work.

Vancouver Island suffered a ~9.0 earthquake in 1700. The evidence suggests that it took place at about 9 p.m. on January 26, 1700 (NS). Although there were no written records in the region at the time, the earthquake's precise time is nevertheless known from Japanese records of a tsunami that has not been tied to any other Pacific Rim earthquake. Long live irony.

The City of Richmond assures residents that buildings are safe, even considering the risk of liquefaction of the soil. Relax, your lives are safe. Your 1.5 million dollar house will be cracked and bit sunken in.

The Sun took the survey route, pointing out that residents don't believe their municipalities are prepared. This doesn't mean they aren't, just that people don't have faith.

The Times Colonist in Victoria takes a pablum approach. I especially like the close: She suggests the public visit the Provincial Emergency Program website at pep.bc.ca, or go to the "public health" section of www.viha.ca should an event occur. If it's a significant event, I'm not sure that's going to work.

Vancouver Island suffered a ~9.0 earthquake in 1700. The evidence suggests that it took place at about 9 p.m. on January 26, 1700 (NS). Although there were no written records in the region at the time, the earthquake's precise time is nevertheless known from Japanese records of a tsunami that has not been tied to any other Pacific Rim earthquake. Long live irony.

The City of Richmond assures residents that buildings are safe, even considering the risk of liquefaction of the soil. Relax, your lives are safe. Your 1.5 million dollar house will be cracked and bit sunken in.

Monday, March 21, 2011

Prosper Australia Calls a Top

Prosper Australia calls a top and tries to get up a grass roots campaign to warn first time buyers to avoid the market.

Prosper Calls For Buyers Strike

Hat tip mflat at VCI

Prosper Calls For Buyers Strike

RP Data reports there are over 900 Melbourne auctions scheduled for the weekend and 2700 over the next three weeks. Prosper believes this enough to decisively tip the market into oversupply.

“I remind you there are 1.3 million Australians with negatively geared rental properties. They are diverting all rents and some personal income to meeting interest payment in the hope of capital gains. When only capital losses are expected, investors will flood the market and overwhelm demand. Buyers will step back, making it virtually impossible to sell at any price.That would be the rational response. You'd be surprised how many owners at the start of a downturn hold off the market "until prices recover" because they cannot stomach the loss they know and are willing to gamble on future unknowable losses. A lot of them will do this. And then a year or two later they mail the keys to the bank. But enough will dump immediately. Especially those not selling at a loss, but realizing they are about to miss their last chance to lock in profits.

Hat tip mflat at VCI

Sunday, March 20, 2011

March 13 Clearance Rates Drop

Uncertainty and/or better reporting has hit the Australian market, breaking Melbourne's upward trend and putting it in line with Sydney.

| Austrian Clearance Rates March 13, 2011 |

Shanghai Real Estate Activity Slows Significantly in February

Big players give a miss to Shanghai realty fair

Statistics from Century 21 China Real Estate in Shanghai, a housing consultancy firm, show that in February, a total of 7,900 units of second-hand apartments were sold, a decline of 62.3 percent month-on-month.

Recently, an online survey jointly conducted by Sina.com and the Oriental Morning Post showed that 51 percent of netizens believe house prices may fall, and 41.2 percent of them feel that now is not a good time to buy a house.

About 172,000 sq m of newly built houses were transacted in February, the lowest since the foundation of the online Shanghai Real Estate Trading Center in May 2004. The average price of the houses dropped 8.8 percent month-on-month to 20,946 yuan ($3,188) per sq m during the same time.

Friday, March 18, 2011

China Price Gains Slow and Another Reserve Requirement Hike

China property inflation edges down, hit by tightening

China hikes banks’ reserve requirements

New home prices in 70 major Chinese cities rose 5.7 percent in February from a year earlier, down from an annual rise of 5.9 percent in January, according to a Reuters weighted average of official data published on Friday.Reuters has their own index as of this year since the Chinese statistics agency has ceased publishing their own.

On a month-on-month basis, property inflation was more muted.

Nationwide, prices were up 0.4 percent, compared with a 0.8 percent increase in January, according to the Reuters calculations.

China hikes banks’ reserve requirements

The nation’s biggest banks must set aside 20% of deposits as reserves with the central bank beginning from March 25, the People’s Bank of China said in an early evening statement.

Wednesday, March 16, 2011

Australian Auction Clearance Rates Strong but Stock Levels Rising

Questions about the veracity of the numbers aside, here is the first week of March in chart form.

Auctions strong in Sydney but high stock levels tipped to keep prices down

(Note that this article is about the following week's activity.)

| Australian House Auction Clearance Rates for Mar 6, 2011 |

Auctions strong in Sydney but high stock levels tipped to keep prices down

(Note that this article is about the following week's activity.)

"When you make an adjustment for the unreported figures, you still get a good result at about 56-58%, so it was a reasonably strong weekend."

"In terms of the last few weekends, they've ranged from the low 60s down to the low 50s. So this is conducive of a market that's not falling by any means, but it's not really taking off either."

SQM's figures show national stock levels have risen 46.1% since February 2010, and are now at a two-year high. While Melbourne recorded the highest stock levels at 37,911, followed by Brisbane at 28,937, Sydney actually recorded the highest month-on-month growth at 15.6%.

Tuesday, March 15, 2011

Vancouver Propping Up National Prices

It's obvious that this is happening, but surprising to see it in the mainstream press. They do not directly point out that demand has been pulled forward, just warn that after the amortization rule changes there will be a drop-off in activity, a critical distinction.

Also, the article deals with averages, which will be all the more skewed.

Vancouver cushions Canada Feb home resales fall

Also, the article deals with averages, which will be all the more skewed.

Vancouver cushions Canada Feb home resales fall

But because of the strength in the heavily weighted Vancouver area -- where the average home price, at C$790,380, was more than double the national average -- national sales did not fall as much as they could have.

. . .

"When you take Vancouver out of the equation, the year-over-year increase in the national average price drops to 3.4 percent," said Gregory Klump, CREA's chief economist.

Sales in February were down 5.9 percent from a year earlier, the smallest year-over-year decline in nine months.

The number of new listings edged up 1.5 percent from the previous month on a seasonally adjusted basis, building on a 4.3 percent monthly increase in January.

Sunday, March 13, 2011

Wen Jiabao Promises Welfare Apartments Will Lower House Prices

Premier: Welfare apartments key measure to curb housing prices in China

Wen Jiabao thinks that someone who qualifies for a welfare apartment would also buy three others costing 150k and leave them empty?

Of course, his words/actions are all about stability not about confusing two distinctive markets for housing. If his promise is kept, the demand for construction materials won't be slacking as quite as far as the hedge funds betting against china think they will.

"Speeding up the construction of welfare apartments is a key measure to curb housing prices. It will cut demand and help solve the problem of the real estate market," he said.

China will build 10 million welfare apartments respectively in 2011 and 2012. A total of 36 million welfare apartments will be built from 2011 to 2015, Wen said.

Wen Jiabao thinks that someone who qualifies for a welfare apartment would also buy three others costing 150k and leave them empty?

Of course, his words/actions are all about stability not about confusing two distinctive markets for housing. If his promise is kept, the demand for construction materials won't be slacking as quite as far as the hedge funds betting against china think they will.

Friday, March 11, 2011

Tuesday, March 8, 2011

China in Summary

Long article from Canadian Business Online

China's coming collapse

"Shell game" doesn't actually cover it. "Ponzi scheme" would be a better choice. Or "musical chairs" except where there are 4 chairs and 100 participants and someone has spilled gasoline on the floor and half the players are chain smokers. That might cover it.

Hat tip to Jimbo at VCI.

China's coming collapse

How could there be so many new buildings going up when, at the same time, so many others already sit empty? Simple. China is engaged in an elaborate shell game to hide a mountain of bad debts piling up on the balance sheets of its banks, developers and state–owned enterprises. In the case of real estate, it's a matter of turning a blind eye to staggering losses, says Patrick Chovanec, a professor at Tsinghua University's School of Economics and Management in Beijing. In an interview last year, he pointed to situations where buildings sit half empty, yet landlords refuse to lower their rental rates. To do so would sink the value of the underlying land, which was used as collateral for the developer's loans. "The rational response would be to lower the rental asking price, but that would mean the value of the collateral would be lowered and the bank would be forced to write down the loan," he says. "So the building stays empty. Economically it makes no sense."

This same scenario is playing out across the country on a massive scale, say experts.

"Shell game" doesn't actually cover it. "Ponzi scheme" would be a better choice. Or "musical chairs" except where there are 4 chairs and 100 participants and someone has spilled gasoline on the floor and half the players are chain smokers. That might cover it.

The list goes on and on. But for how much longer, wonder some China watchers. The rush to build over the past five years has left China drowning in overcapacity in many key sectors. In Liaoning province, the government is spending hundreds of millions of dollars to build five mega–ports over the next couple of years, even though China's ports are already operating far below capacity. Likewise, according to a report by Pivot Capital Management that analyzed China's manufacturing capabilities, China continues to build new steel mills, cement factories and aluminum smelters even though up to one–third of existing plants sit idle.

In plain terms, should China's economic miracle turn out to be a mirage, all of that would be at risk. "If China fails, or even if this fixed investment model fails, countries like Australia and Canada are in deep trouble," says John Lee, a foreign–policy expert at the Hudson Institute who is also a research fellow at the Centre for Independent Studies in Sydney, Australia. For one thing, commodity prices are likely to plunge. That could throw a wrench in plans for the oilsands, which require high oil prices to remain profitable, and crimp much of the manic exploration activity in mining. Canada's resource sector was one of the primary drivers for employment over the past decade, according to Statistics Canada, so a correction in China would also rob this country of a key engine for job growth. It would also sap provincial and federal governments of needed tax and royalty revenue, hurting their balance sheets.

Hat tip to Jimbo at VCI.

Monday, March 7, 2011

Chinese Buying Up the World's Shelter

More mainland Chinese investing in Singapore property

How much of this money is leaving China legally? And will a future cash-strapped government try to track it down?

Mainland Chinese buyers are now the second largest group of foreigners who buy homes in Singapore, falling behind to Malaysian buyers - who have typically dominated foreign ownership of property here.

Chinese buyers accounted for 23 per cent of foreign buyers in the fourth quarter of 2010, up 3 percentage points from the previous quarter.

How much of this money is leaving China legally? And will a future cash-strapped government try to track it down?

Sunday, March 6, 2011

Accusations of Underreporting of Failed Auctions in Australia

Auction rates fudged by failed campaigns

The numbers do seem to have made a remarkable recovery from the long slow slide last year.

EMBARRASSED agents are covering up a growing failure to sell homes at auction by not telling reporting bodies about their failed campaigns.

Figures compiled by research agencies Australian Property Monitors and Residex over the past three weeks show that between 10 per cent and almost 50 per cent of auction results across Sydney went unrecorded.

Cooley Auctions had a 51 per cent clearance rate for its 76 auctions last Saturday, the busiest day of the 2011 selling season so far, compared to APM's 65 per cent clearance rate for the day.

"Ours is 100 per cent accurate as we represented 12.2 per cent of the market on that day, so I find it hard to believe there's a 14 per cent difference across the market," Mr Cooley said.

Cooley Auctions also recorded a lower clearance rate of 55 per cent for the entire month of February than APM's 62 per cent.

The numbers do seem to have made a remarkable recovery from the long slow slide last year.

Hey, Economist, Prices Aren't Too High, Rents Are Too Low!

I missed Friday Point and Laugh day. Sunday will have to do.

Don't believe the reports on Australian house values

You rebutted your own first point, so nowhere to go with that. And your last point is the corollary to Really, we're the size of the continental U.S. with 7% of the population, but we're running out of space, honest!

Hattip to CanuckDownUnder at VCI

Don't believe the reports on Australian house values

But hold it one second … what exactly did The Economist measure? The ratio of home prices to rents in 20 economies.Yeah, that pesky measure that every housing bubble always reverts to.

It's a single measure - and a leaky one at that.

You could simply say Australia tops The Economist list because our average rents are too low - rental yields have remained unchanged at about 4 per cent for many years, though they are beginning to rise.See, I didn't make that headline up. In case you had already accused me of doing so. Understandably.

More likely our home values are justified by one of the best economies in the developed world - even if it is a two-speed model in which mining industries thrive and other sectors struggle. And that's before you factor in the exceptional tax shelter encased in the family home along with the concentration of our populations in four cities.Do you write for a comedy programme, sir? You really should.

You rebutted your own first point, so nowhere to go with that. And your last point is the corollary to Really, we're the size of the continental U.S. with 7% of the population, but we're running out of space, honest!

What's more, the factors that could start to immediately move prices - higher or lower - are dormant. Investors as a proportion of the market have remained unchanged since the GFC while the housing shortage remains virtually static.You wrote it, but do you even know what it means? Is there some reason you aren't just speaking plainly? I bet you dimes to dollars you skipped counting the spate of barely regulated foreign buyers as investors, but you weren't specific enough here to expose your argument to real debate.

Indeed, the floods highlight the problem with housing statistics. The statistics are riddled with localised exceptions.You're doing it again. Restated: I have an excuse for why my logic doesn't hold up for every instance where you might actually start pointing out specific numbers.

But there are few signs that prices are now going to plunge.You heard it here first, people. And see how easy it is to say something right out. Oh, except now you're going to be held to that. No one's going to hold you to what you said above, because they don't know what it means.

It is much more probable that they will drift for at least a year after slipping by an estimated 1 per cent in the 12 months to January. And this is not a bad outcome for most homeowners whatever this report or the next report might care to say.Uh oh. According to RP Data's Rismark Index Capital city values were down -1.6 per cent (s.a.) while the rest-of-state markets saw a -1.2% (s.a.) tapering in values. That's just for January. (Admittedly a noisy month. Maybe February will rescue our heroic cheerleader yet. Stay tuned.)

Hattip to CanuckDownUnder at VCI

Saturday, March 5, 2011

Bottom Line Manageable Decline in China is 30%

CHINA NPC: China Banking Regulator: Maximum Fall Of 30% For Property Prices Acceptable

Raise your hand if you think China has any top tier cities that are only 43% overvalued.

Eh, so what, the central government will just use all that cash to bail out the banks, right? In one of his interviews, Chanos insists those holdings are tied up in sterilizing the exchange rate and aren't actually available. I have a feeling we'll be finding out.

BEIJING (Dow Jones)--Stress tests found the scope of risk from real-estate loans in China is controllable, but the "bottom line" for a fall in real-estate prices is 30%, China Banking Regulatory Commission Assistant Chairman Yan Qingmin said Saturday.

Raise your hand if you think China has any top tier cities that are only 43% overvalued.

Eh, so what, the central government will just use all that cash to bail out the banks, right? In one of his interviews, Chanos insists those holdings are tied up in sterilizing the exchange rate and aren't actually available. I have a feeling we'll be finding out.

Hot Hot Hot

Revisiting the Vancouver numbers. Here is the updated Year on Year price change graph. Not much to observe beyond the whiplash, but Detached pulled up harder than Overall.

The next question one might ask is: Is the price change evenly distributed?

Well, no. And if you are the type who sees Mainland Chinese buyers when you close your eyes at night, you will not be surprised by what areas come out on top.

So, what is left if we take out the super hot markets? I weighted the percent changes by the number of sales and the recomputed. NOTE: I couldn't get the overall number to match. When I took each of the sub-market percent changes and weighted them against the total sales last month and recalculated the overall percent change I got 8.29% rather than 5.98% which is what you get if you take the overall HPI from this month and compare it to the overall HPI from a year ago last month. I spent quite a bit of time trying to figure out where that's coming from, but could not. (I'm inclined to guess there are some halo areas not included in the sub-market breakouts, but I don't know that for certain. It would, however, explain why the overall number is lower. The other possibility is the total sales in certain areas does not accurately reflect the actual "typical" sales used to calculate the HPI for that submarket.)

I think the calculations below are illustrative within the scope of just the data presented below. But it can't be compared to the overall historically reported numbers. It does serve to illustrate the scale of the change we get if we exclude certain submarkets. But that's all.

Note: Sunshine Coast is such a small number of sales it barely matters if it's in or out.

Note: Sunshine Coast is such a small number of sales it barely matters if it's in or out.

The next question one might ask is: Is the price change evenly distributed?

Well, no. And if you are the type who sees Mainland Chinese buyers when you close your eyes at night, you will not be surprised by what areas come out on top.

So, what is left if we take out the super hot markets? I weighted the percent changes by the number of sales and the recomputed. NOTE: I couldn't get the overall number to match. When I took each of the sub-market percent changes and weighted them against the total sales last month and recalculated the overall percent change I got 8.29% rather than 5.98% which is what you get if you take the overall HPI from this month and compare it to the overall HPI from a year ago last month. I spent quite a bit of time trying to figure out where that's coming from, but could not. (I'm inclined to guess there are some halo areas not included in the sub-market breakouts, but I don't know that for certain. It would, however, explain why the overall number is lower. The other possibility is the total sales in certain areas does not accurately reflect the actual "typical" sales used to calculate the HPI for that submarket.)

I think the calculations below are illustrative within the scope of just the data presented below. But it can't be compared to the overall historically reported numbers. It does serve to illustrate the scale of the change we get if we exclude certain submarkets. But that's all.

Wednesday, March 2, 2011

Seriously Juiced Market

Vancouver detached sales up 43% from last year.

February 2011

REBGV reports increased housing demand in February

Up $222,000 since November 2010. I don't know what y'all are smokin' . . .

Sellers showed up to the party too. More new listings than last year and higher total listings.

It's unfortunate they don't break down the number of sales by area. If the entire extra block of sales were in Van West and Richmond, that would be a different situation than the sales being spread out evenly. Oddly, the HPI has not yet been published, nor do they mention the overall HPI number on the report. I'll update charts when that comes out.

February 2011

REBGV reports increased housing demand in February

Between November 2010 and February 2011, the MLSLink® Housing Price Index (HPI) benchmark price of a detached home in Richmond increased $190,739 to $1,099,679; in Vancouver West, detached home prices increased $222,185 to $1,850,072. In comparison, detached home prices across the region increased $51,762 between November 2010 and February 2011 to $848,645.

Up $222,000 since November 2010. I don't know what y'all are smokin' . . .

Sellers showed up to the party too. More new listings than last year and higher total listings.

It's unfortunate they don't break down the number of sales by area. If the entire extra block of sales were in Van West and Richmond, that would be a different situation than the sales being spread out evenly. Oddly, the HPI has not yet been published, nor do they mention the overall HPI number on the report. I'll update charts when that comes out.

Tuesday, March 1, 2011

China House Prices up 0.5% in February

I love that quickly published data.

China February Residential Property Prices Up 0.48% Vs January - Data Provider

Is this the long awaited slowdown? Hard to say. Short month. Secondly, January with the New Year imminent was a big time for getting financing (the government made extra noises about keeping that under control). I'm not convinced that the pre New Year spree didn't simply pull some demand forward.

China February Residential Property Prices Up 0.48% Vs January - Data Provider

China Real Estate Index System said that 80 cities showed month-on-month increase in property prices, while 18 cities posted a decline in property prices over the same period, and the remaining two cities showed no change. 78 cities posted price increases of less than 1%, it added.

Is this the long awaited slowdown? Hard to say. Short month. Secondly, January with the New Year imminent was a big time for getting financing (the government made extra noises about keeping that under control). I'm not convinced that the pre New Year spree didn't simply pull some demand forward.

Subscribe to:

Posts (Atom)