Roubini sees housing prices getting out of whack in quite a few small and mid-sized nations that are well-governed and managed to avoid the worst economic effects of the financial crisis: Switzerland, Sweden, Norway, Finland, France, Germany, Canada, Australia, New Zealand and the London metropolitan area in the U.K. He adds some key emerging markets that show the same dynamic: Hong Kong, Singapore, China and Israel, and major urban centers in Turkey, Indonesia, India and Brazil.Hat Tip: 4SlicesofCheese at Vancouvercondo.info

Friday, December 6, 2013

17 Countries with Housing Bubbles

According to Nouriel Roubini, cheap credit is driving up prices in some smaller (and not so small) markets.

These 17 countries may have housing bubbles. If they pop, God help us all.

Tuesday, October 22, 2013

London prices hit new highs on "frenzy"

Overseas investors are in a "frenzy".

London house prices at new high

Asking prices in London saw an "unsustainable" 10 per cent month-on-month increase in October, pushing typical asking prices in the capital to STG544,232, leapfrogging a previous high set in July by more than STG28,000.

Prices across the country are 3.8 per cent higher than they were a year ago, although in London they have shot up by 13.8 per cent over this period, Rightmove said.

Monday, October 21, 2013

House prices in Netherlands down 4%, return to 2003 levels

September Data from Netherlands CBS

Prices for September are down over 4% year on year, a moderating of the fall that was -10% mid-summer.

Rabobank thinks housing is undervalued

by 25 to 30 percent, and that prices will recover in another year. But admits that mortgage debt is already among the highest in Europe.

Worth noting that a gain of 30% would more than wipe out the entire decline since the change in world credit spurred by the crisis and would send prices to new highs.

Here are Dutch house prices against average income compared to Britain and US. You can decide if this looks undervalued and ripe for a rise.

Prices for September are down over 4% year on year, a moderating of the fall that was -10% mid-summer.

Prices of existing owner-occupied dwellings were at the same level in September 2013 as in early 2003. They were 19.6 percent below the record level registered in August 2008.

Rabobank thinks housing is undervalued

by 25 to 30 percent, and that prices will recover in another year. But admits that mortgage debt is already among the highest in Europe.

Worth noting that a gain of 30% would more than wipe out the entire decline since the change in world credit spurred by the crisis and would send prices to new highs.

Here are Dutch house prices against average income compared to Britain and US. You can decide if this looks undervalued and ripe for a rise.

Sunday, October 20, 2013

Real Estate Highlights of Credit Suisse Wealth Report

Global Wealth 2013

India

India

Along with most countries in the developing world, personal wealth in India is heavily skewed towards property and other real assets, which make up 86% of household assets.France

Much of the pre-2007 rise was due to the appreciation of the euro against the US dollar. However, France also experienced a rapid rise in house prices, as a result of which real property now accounts for about two-thirds of household assets. Personal debts are just 12% of household assets, a relatively low ratio for a developed economy..Australia

nterestingly, the composition of wealth is heavily skewed towards real assets, which amount on average to USD 294,100 and form 59% of gross household assets. This average level of real assets is the second highest in the world after Norway. In part, it reflects a sparsely populated country with a large endowment of land and natural resources, but it is also a manifestation of high urban real estate prices.Canada

The long-term rise in real estate was interrupted only briefly, and since 2008 the market has seen both new construction and house price increases. Rapid growth in mortgages has fuelled a continuing rise in household debt. Mortgage terms were tightened in 2012 and the market cooled somewhat, but there are continuing concerns. It is not clear whether the final landing will be soft or hard.

Thursday, October 17, 2013

Dubai renewed boom spurs calls to remember the crisis

Dubai property sector comeback stirs fears of new bubble

Some residential property has bounced by about 20 percent, said Alan Robertson, chief executive officer for the Middle East-North Africa region at Jones Lang LaSalle property consultancy.

"We think prices will continue to grow quite quickly over the next 12 months, but over the next 24 months we will see the rate of growth slow down," he told AFP, adding that prices were still 20 to 30 percent below their 2008 peak.

Parable for the Spanish Bubble, Deer take over 37 million euro estate

Two years ago the

37-million euro Spanish hunting lodge overrun by deer a parable of property bust

Now, just two years after he lost the property to the bank, wild sheep roam at will and with no hunting, the deer population has multiplied more than fivefold, said Fabian Vinagre, the caretaker of the estate near the Spanish city of Caceres 305 kilometers (190 miles) west of Madrid.

Sareb’s sell-off is part of the process of Spain’s recovery from a five-year slump that caused property prices to plunge more than 30% and drove default rates on loans for real estate activity as high as 31%.

Even so, Spain’s property market slump is still deep. House sales fell 15% in August from a year earlier and home- mortgage approvals fell an annual 43% in July, according to Spain’s National Statistics Institute. Fitch Ratings said today the non-performing loan ratio for mortgages increased to 5.2% from 4.1% last quarter.

Monday, October 14, 2013

Home Loan Approvals in Australia drop 4%

Australia Home Loans Fall, Tempering Housing Recovery

Record-low interest rates have fueled a recovery in rate-sensitive sectors like housing, with auction clearances, house prices, and homebuilding permits all increasing in recent months. Home loans have also risen steadily up to now. Cementing recent signs that much of the housing market activity is being driven by investors, first-time homebuyers accounted for less than 14% of the market in August--the lowest percentage in nearly a decade. New lending to investors was flat on-month, but surged by almost 26% from a year earlier, the steepest gain since 2007.Deutsche Bank also believes the rise is investor driven. New records were set in Sydney and Melbourne, fueled by eight rate cuts since end of 2011.

Sunday, October 13, 2013

Foreclosures in Wenzhou strain guarantee companies

15,000 foreclosed properties in Wenzhou pummeling guarantee companies

Nosedives in the Wenzhou property market of up to 50% have forced some property buyers to stop making payments to the lenders and drop their guarantees to companies as their mortgages have exceeded the property's market value. Many have literally abandoned property, a tremendous fallout for the city's 300 surviving guarantee companies,

The 300 guarantee companies capitalized on the "residual value of collateral," using the remaining quota in a property mortgage to leverage a second mortgage. For example, banks, out of safety concerns, typically approved a mortgage of about 60% of the evaluated value of the property, with 40% untouched. Guarantee companies will try to offer mortgages for the remaining 40%, and claim a service fee. The entire operation relies heavily on a stable property market.

Monday, July 29, 2013

On Falling Interest Rates Driving a House Price "boomlet" in Australia

The Absurdity of Australian Property

So on this basis, you would argue that Sydney has moved ahead of its fundamentals over the past 12 months while Melbourne has actually underperformed. But with lower interest rates, and the prospect of more cuts to come, you could also argue that Sydney’s strong house prices reflect the discounting of a lower interest rate environment.

On the other hand, you have to ask yourself why interest rates are expected to fall. It’s because of a slowing economy. It’s because of fears over the growth prospects of our largest trading partner, China, which hasn’t even began to reform its hopelessly imbalanced economy yet.

Looking at it from a psychological perspective, you could argue that buoyant activity in the market is a result of a ‘throwing in the towel’ mentality of previously reluctant buyers, as well as continued involvement from the legion of property players in Australia who have never experienced a downturn, and who believe we will never see one again.

Friday, July 26, 2013

Shadow Banking in China is a Symptom

Shadow banking as the symptom and not the disease

How interest rate controls created a shadow banking system in China

Why do these exist and why do regulators tolerate them? As Zhang rightly points out and a few commentators observed post-Saradha, shutting down shadow banks can be done but amounts to shooting the messenger. The real culprit is financial repression. In the absence of high-quality, formal options to save, invest and borrow, people are forced to deal with the more “shadowy” segments of the financial system. In its extreme form, investments in financial assets of any form are rejected in favour of physical assets. In its Financial Stability Report, RBI acknowledges that “the shift from financial assets to real estate and gold has become stark. Inflation, low penetration of banking services, credibility of financial institutions in the wake of mis-selling of products and financial frauds, low post-tax returns on bank deposits, negative/low real interest rates etc could be some of the issues that need to be addressed to re-direct non-financial savings towards financial savings”.And the South China Morning Post

How interest rate controls created a shadow banking system in China

As a result, some depositors would like to receive a higher rate. At the same time, some borrowers and banks are willing to pay higher rates, because they can still make a profit on the higher rates. Thus the policy has created a shadow banking system paying a higher rate of interest than the official rate.

This is causing concern that these wealth management products are being used to "repackage old loans and prop up risky companies and projects", and that "shadow banking is helping drive the rapid growth of credit in a weakening economy, which could lead to - in the worst situation - a series of bank failures", the report said.This author seems to think that bribery and the black market for money will vanish with liberalization of interest rates. But there will always be borrowers who do not qualify at any interest rate who will bribe for a loan at all or to fudge the rate. State enterprise itself uses its position to obtain unreasonably low rates and always will. Interest rate liberalization will not end corruption, it will squeeze out the middlemen who are repurposing loans for an allowed activity into a banned one, which will remove a level of corruption from large projects. Just because interest rates can float doesn't suddenly mean small business is going to get loans from a state bank.

Wednesday, July 24, 2013

China bans new government buildings for five years

This time they were also smart enough to ban some of the work arounds used to funnel money to construction during previous restrictions.

China Orders Ban on New Government Buildings

Most tallies of total local government debt in China tend to be in the vicinity of $2 trillion, equal to three months of China’s entire economic output, but some estimates are even higher.

“We should put into perspective that the problem of local government spending on buildings is not the most serious problem facing China’s economy,” Mr. Li said in a telephone interview from Beijing. “The property bubble, shadow banking and the state-owned enterprise monopolies are far more risky.”

Sunday, June 23, 2013

Hamilton, ON house prices suffering from substitution effect

Bidding wars, soaring house prices hit Hamilton real estate

Median household income was $79300 using statcan.gc.ca and applying the last 4 years average median increase to the latest data.

Resulting in a median multiple of 4.3x.

Not sustainable, but more interesting in the medium term is what will the fallout be. As Toronto wanes will Hamilton continue to be seen as a boom town and weather the national downturn better, or will a contraction hit harder due to the weaker base to fall back on. If it remains clear that the transport project will finish I expect more of the former.

The former librarians were shocked to discover that for about half the price, $295,000, they could get everything they’d hoped to find in Toronto — a cool condo close to a burgeoning arts scene, thriving cafes, up-and-coming restaurants, and bike paths that meander along a waterfront undergoing a rebirth.

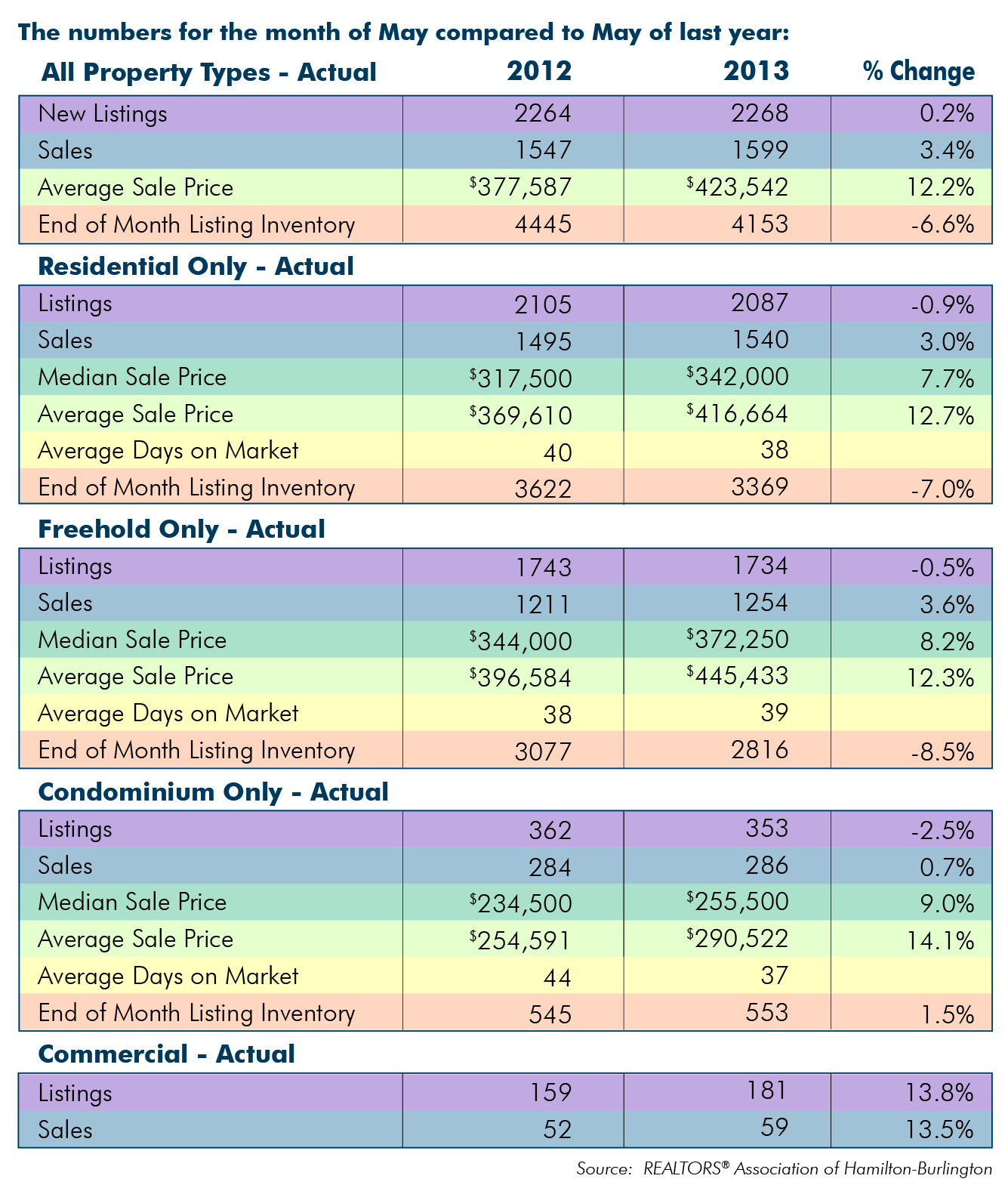

There they discovered elegant, and sometimes unloved, brick Victorians, charming workers’ cottages and even Rosedale-like mansions. And they were all shockingly affordable — at least by Toronto’s sky-high standards.Median price for residential was $342,000 last month according to the RAHB chart for May 2013

{kind=link}

Median household income was $79300 using statcan.gc.ca and applying the last 4 years average median increase to the latest data.

Resulting in a median multiple of 4.3x.

Not sustainable, but more interesting in the medium term is what will the fallout be. As Toronto wanes will Hamilton continue to be seen as a boom town and weather the national downturn better, or will a contraction hit harder due to the weaker base to fall back on. If it remains clear that the transport project will finish I expect more of the former.

Friday, June 21, 2013

A model for future bank bail outs that avoids taxpayers forking over money

Handling of shaky Co-op Group could serve as a model for future bail outs, to henceforth be called "bail-ins",

UK's Co-op Bank agrees to £1.5 billion 'bail-in' rescue plan

Co-op Group, which runs supermarkets, pharmacies and funeral services, will retain a majority stake in the Co-op Bank, which has 4.7 million customers. Sources said bondholders are likely to end up with at least a quarter of the bank's shares.

Sutherland said he was confident a "good proportion" of bondholders would support the move, given that coupons on their debt will be canceled making them effectively worthless. If they refused, the bank would face the threat of nationalization.

Analysts have blamed Co-op Bank's problems on its takeover of the Britannia Building Society in 2009.Like Bank of America and Countrywide it really shows how incompetent bank management can be to not understand how much liability they are "investing" in.

Industry sources say Britannia, which had lent aggressively on commercial property, was likely to have required a taxpayer-bailout had it not been bought by the Co-op.

Co-op said it would hive off toxic assets worth about 14.5 billion pounds into a 'bad bank,' most of which are from Britannia, as part of a restructuring.

Co-op said the bail-in plan will generate 1 billion pounds of new capital this year and 500 million pounds in 2014. This includes a debt-for-equity exchange with the bank's subordinated bondholders.

Tuesday, June 18, 2013

Truck Tonnage Index Indicates U.S. Economy Got a Lift in May

Seasonally adjusted, up 2.3% month on month, 6.7% year on year

By raw numbers up 5.4% month on month. ATA Truck Tonnage Index Surged 2.3% in May

Ad: USDOT Truck markings, decals for commercial haulers

By raw numbers up 5.4% month on month. ATA Truck Tonnage Index Surged 2.3% in May

Some of the increase is attributable to factory output rising in May for the first time since February (+0.2%) and retail sales performing stronger than expected in May (+0.6%). Costello added, "The 6.8% surge in new housing starts during May obviously pushed tonnage up as home construction generates a significant amount of truck tonnage."And some background:

. . .

He added that tonnage continues to outpace the number of loads hauled as heavy freight (e.g., housing construction materials and sand and water for hydraulic fracturing) is outperforming box trailer (i.e., dry van) freight.

Trucking serves as a barometer of the U.S. economy, representing 67% of tonnage carried by all modes of domestic freight transportation, including manufactured and retail goods. Trucks hauled 9.2 billion tons of freight in 2011. Motor carriers collected $603.9 billion, or 80.9% of total revenue earned by all transport modes.

Ad: USDOT Truck markings, decals for commercial haulers

China Credit Bubble is Unprecedented

Total credit has jumped from $9 trillion to $23 trillion since the Lehman crisis and is now 200% of GDP. Each additional Yuan of loans now generates only 0.15 in growth compared to .85 four years ago.

Fitch says China credit bubble unprecedented in modern world history

But now the house of cards is starting to wobble. Trust products are starting to default on their short term loans. $2 Trillion in wealth products act as a shadow banking system allowing banks to end run around regulation.

Fitch says China credit bubble unprecedented in modern world history

"There is no transparency in the shadow banking system, and systemic risk is rising. We have no idea who the borrowers are, who the lenders are, and what the quality of assets is, and this undermines signalling," she told The Daily Telegraph.Large project loans over the last decade are reputed to sometimes have no repayment requirement at all, loans plus accumulated unpaid interest were simply rolled into a new loan.

While the non-performing loan rate of the banks may look benign at just 1pc, this has become irrelevant as trusts, wealth-management funds, offshore vehicles and other forms of irregular lending make up over half of all new credit. "It means nothing if you can off-load any bad asset you want. A lot of the banking exposure to property is not booked as property," she said.

But now the house of cards is starting to wobble. Trust products are starting to default on their short term loans. $2 Trillion in wealth products act as a shadow banking system allowing banks to end run around regulation.

It also flagged worries over an exodus of hot money once the US Federal Reserve starts tightening. "China will face large-scale capital outflows if there is an exit from quantitative easing and the dollar strengthens," it wrote.There are several economies that will be strained when the U.S. ends QE.

The journal said foreign withdrawals from Chinese equity funds were the highest since early 2008 in the week up to June 5, and withdrawals from Hong Kong funds were the most in a decade.

Monday, June 17, 2013

Housing could hobble wider Australian economy

Commodity dependent economy relying on China, seven rate cuts failing to significantly stimulate, banks relying on wholesale funding. Banks have reduced their exposure but still need 85 billion on funding for the next twelve months, 2/3 from offshore. Like Canada, it all falls to the bond markets.

State Street’s ‘Mr. Risk’: Watch Australia’s Housing Market

State Street’s ‘Mr. Risk’: Watch Australia’s Housing Market

Fred Goodwin, a macro strategist at Boston-based State Street, warned on Monday that a steep correction in house prices, while still a low probability, would hobble the ability of Australian banks to raise funds in the bond market given their heavy exposure to mortgages. Such a scenario would choke credit to the wider economy and exacerbate an economic downturn.

His views come as economists from Goldman Sachs GS +1.43% to BNP Paribas BNP.FR +1.09% warn of a growing risk of recession in Australia, a scenario deemed unthinkable even 12 months ago for a country that has enjoyed 21 years of uninterrupted economic expansion.After 21 years of expansion is a long time on one side of the cycle. How does that make it more unthinkable?

Sunday, June 16, 2013

Former Bank of America employees claim homeowners ripped off customer by lying to them about their loan modifications

When literally no one likes a company, it's probably not just all in the customers' heads.

Former Bank of America workers allege it lied to home owners

Former Bank of America workers allege it lied to home owners

The bank allegedly used these tactics [lying about status and denying modifications to qualified applicants] to shepherd homeowners into foreclosure, as well as in-house loan modifications. Both yielded the bank more profits than the government-sponsored Home Affordable Modification Program, according to documents recently filed as part of a lawsuit in Massachusetts federal court.

For example, an employee who placed 10 or more accounts into foreclosure a month could get a $500 bonus. At the same time, the bank punished those who did not make the numbers or objected to its tactics with discipline, including firing.What does it take to justify making this bank cease to exist? It is not a benefit to banking, the country, the markets, or customers. Or taxpayers.

. . .

The testimony from the former employees also alleges the bank falsified information it gave the government, saying it had given out HAMP loan modifications when it had not.

The court documents paint a picture of customer service operations where managers roamed the floor with headsets, able to listen into any call without warning. Service representatives were told to lie to homeowners, telling them their paperwork and payments had not been received, when in reality they had.

Friday, May 24, 2013

Visualizing losses on house sales

Squaring house prices

Interesting visualization showing the loss plotted against the year of purchase and year of sale in England and Wales.

Interesting visualization showing the loss plotted against the year of purchase and year of sale in England and Wales.

|

| Graph from Economist.com |

Chinese influence on Australian Housing Bubble

Australian Housing Bubble Has Chinese Overtones

Australians have gone heavily into debt to buy houses that cost more than ever, especially the land component; and there's no sign this trend will end anytime soon. Mortgage debt has more than quadrupled from 19% of GDP in 1990 to 84% in 2012-- as high as that of the U.S. at its peak where mortgage debt as a percentage of GDP has fallen from 86% in 2009 to 68% in 2012. Negative gearing and easy lending combined to push house prices higher. Looking at affordability as a function of disposable income, both the ratio of total debt and interest payments to disposable income are very high - see the chart below. Widespread mortgage fraud to gain bank credit is asserted by Denise Brailey, the president of the Banking and Finance Consumer Support Association (an organization dedicated to protecting the public against predatory financiers).

|

| Graph from Seeking Alpha |

Australia's economy is experiencing increasing reliance on overseas funding, becoming more interlinked with China's growth and business cycle. The Chinese economy grew at 7.8% GDP in 2012, the slowest since 1999, and an increase in global commodity supplies could cause a sharp reduction in Australia's incomes and employment. Australia linked up with China in direct currency trading in March and this puts the country in a tenuous position if trade between the two countries slowed dramatically and would prompt a severe correction of home prices which some feel could take price all the way back to the 1990's.

Sunday, April 28, 2013

China jails 1400 for loan sharking

China jails over 1,400 in loan-shark crackdown

People netted in the crackdown were convicted of violations including public advertising to find lenders and promising excessively high rates of return, Du said at a news conference. He gave no details. Legal experts say loans between individuals are legal and the government has failed to make clear what lenders and borrowers are allowed to do.Loan sharks have a more balanced two-sided relationship with "clients" than the term implies in the west. They are known as much, or perhaps more so, as a means to invest for outsized returns than they are as place for the desperate to borrow. So this crackdown could theoretically been entirely over fundraising.

"Banks are offering fewer loans, because the bad loan rate is rising," said Zhou. "It is harder to get underground loans, too. People are more afraid of running the risk of lending money.

Thursday, April 18, 2013

GDP growth is slowing while credit expands -- is China facing a great economic wall?

Has China's Economy Hit a ‘Dead End’?

Hat tip: Painted Turtle commenting at vancouvercondo.info

Robust credit issuance – which rose by almost 60 percent in the first quarter from a year earlier – is no longer able to generate the same level of growth as it did compared to a decade ago, said analysts.While the manufacturing index has returned to positive territory: China Manufacturing Index Hits 11 Month High

Back in the mid-2000s, one yuan of credit generated around one yuan of nominal GDP. In 2012, three yuan of credit generated around 1 yuan of nominal GDP, according to financial analysis firm IHS.

The purchasing managers index, a measure of economic expansion and contraction, reached 50.9 in March, slightly above the equilibrium mark of 50. It was 50.4 in January and 50.1 in February and has now remained above 50 for six consecutive months.The CNBC article goes on to say:

Of the data released on Monday, economists say the most telling indicator of weakness in the economy is the deceleration in industrial production in March to 8.9 percent from an expected increase of over 10 percent. In August 2012 when hard landing fears were running high industrial production also grew at the same pace.

"We have lost confidence in a robust recovery," added Alistair Thornton, senior China economist at IHSThis IS the recovery. China's economy is a giant snake still digesting the bulk of the post crisis bailouts. Now we are just waiting around to see how skinny the snake really is without being force fed.

"While August 2012 proved the bottom for last year's downturn, we doubt March will be the turning-point for 2013, given macro policy has shifted to a tighter stance with renewed controls on the housing market, local government financing vehicles and wealth management products," Thornton said.Okay, this is an unexpectedly short economic cycle (based on the calendar year?) being analyzed here. I don't know where to go with that.

Hat tip: Painted Turtle commenting at vancouvercondo.info

Canadian Revenue Crackdown on Condo Flips

Long overdue. Lots of anecdotal evidence tax dodging in flipped assignments is widespread. If so, just wind of a crackdown will put a damper on speculative sales.

Currently there are three tiers:

No tax on gains from sales of primary residence.

Tax on half the gain from selling a recreational, rental, or investment property.

Full tax for making a business of real estate investment.

Some Toronto condo sales face CRA scrutiny

Currently there are three tiers:

No tax on gains from sales of primary residence.

Tax on half the gain from selling a recreational, rental, or investment property.

Full tax for making a business of real estate investment.

Some Toronto condo sales face CRA scrutiny

The CRA has yet to disclose how many sellers have been affected. But Toronto tax lawyer and text author David Sherman and other tax experts, accuse auditors of unfairly ignoring some legitimate explanations for sales. Meanwhile, Finance Minister Jim Flaherty wants the CRA to collect more than $500 million extra from suspected tax cheats this year.

“The auditors have applied a rare 50 per cent penalty for ‘gross negligence,’ even on those who had never owned a condo previously,” says Sherman.Sure sounds like they want to make a point about the seriousness here, not just collect the tax.

One of Rhodes’ clients was single when he bought a condo in downtown Toronto in 2005. By 2009 he was engaged, and his fiancée wanted to be closer to her work in Guelph. So, he sold it, soon after it was registered. An auditor decided that the sale so soon after registration was suspicious, and so was the original choice of a two-bedroom apartment: “There is no reason to purchase a two bedroom condominium for one person,” he claimed. Rhodes says his client was assessed with over $100,000 of business income, resulting in a tax bill of roughly $50,000. He also faced a $25,000 penalty. “I estimate the cost to take this to the Tax Court (of Canada) will be around $10,000 to $15,000.”It will be interesting to see if the decisions from this crackdown stand. Real estate seems to get its way on these things. Given the long timeline between condo sales and registration, most everyone could come up with a life excuse for bailing.

Wednesday, April 17, 2013

Kung Fu fighting against developer

Chinese Kung Fu Expert Beats Up Men Who Came To Evict Him From Home

At first, the property company stuck up posters warning of dire consequences for any families who held out. Then, Mr Shen said, when 70 of the 100 households had left, the threats escalated. "This mob of thugs would block the street most days. They would pick on the women, threatening to kill their kids. Then people started tossing bricks through windows and letting off fireworks at night. Some people got beaten on the street."Shen went to Beijing and after a call from the Central Military Commission has been unreachable.

On October 29, as Mr Shen went to work and his wife popped out for a packet of instant noodles, a mob of "30 to 50 men" materialised at their front door. "My wife tried to close the door, but they pushed it back and she tripped over. That is how the fight started," said Mr Shen. With a flurry of kicks and punches, he and his 18-year-old son, a fellow kung fu devotee, set about the attackers, rendering seven of them near unconscious in the hallway.

Sunday, April 14, 2013

Cocaine contributed to the financial crisis

Financial crisis caused by too many bankers taking cocaine, says former drugs tsar

Prof Nutt said that too many bankers who took the drug were “overconfident” and so “took more risks” and said that not only did it lead to the current crisis in this country, but also the 1995 collapse of Barings bank. He said cocaine was perfect for their "culture of excitement and drive and more and more and more", adding: “Bankers use cocaine and got us into this terrible mess. It is a 'more' drug."

Wednesday, April 10, 2013

Condo Developers in Toronto backing off

Toronto Condo Kings Retreating to Avert Crash: Mortages

“Most developers have their hands in their pockets right now,” said Brad Lamb, president of Brad J. Lamb Realty Inc., a developer and the city’s largest condominium broker. His firm, which is marketing more than 45 high-rise developments in the city, won’t start a new project until 2014, Lamb said in an interview at Bloomberg’s office in Toronto. Lamb said he has eight projects in Toronto and Ottawa “on the drawing board.”

The supply of new high-rise units reached 21,262 in February, 34 percent more than the same period a year ago and close to a record 21,696 in October 2012, RealNet figures show. About 61,000 units are currently under construction -- the most ever -- and a record 35,757 residential units will come on stream next year, RealNet said.

Sales of high-rise homes in the city have dropped 34 percent since 2011, after rising 64 percent in the past decade until 2012. Prices have declined 5.5 percent over the past two years, according to RealNet.Rising supply facing the headwind of sharply declining sales this year, implies this move is too late. Hat tip: vangrl posting at vancouvercondo.info

Wednesday, April 3, 2013

An Australian Housing Recovery without a Construction Recovery?

There will be no housing recovery until there is a construction recovery: Catherine Cashmore

Albeit – do not mistake this for a market recovery – once again, it’s all confined to the established sector. Everyone is effectively fighting over the same pool of existing dwellings in a never ending game of 'musical chairs.' We’re simply paying higher prices for an ageing stock of second hand homes.

Indeed, there’ll be no housing recovery until we have a construction recovery. As the first ABS building approvals update for 2013 indicated, approvals in January fell for a second consecutive month, lingering back below the 13,000 mark.

Spokesperson for the HIA, Harley Dale, commented that even with a rise of 3.3% in detached house approval, overall approvals for this sector are still down by 1% over the three months to January 2013.

Fletcher Building LTD is also flagging the weight of the issue, stressing that the ongoing weakness in Australia's new housing sector is likely to last until the end of the year. Along with the others, they are crying for lower rates and a return of incentives for first-home buyers.

Tuesday, April 2, 2013

Exposure to housing could come back to bite Australia

The proportion of total loans in Australian banks is now 59%, up from 24% in 1990.

Exposure to housing could come back to bite us

Cross-country comparisons of house prices against incomes and rents are inherently problematic, but comparing the total value of a nation's housing stock against the size of its economy makes for a more useful comparison.

Australia's ratio of housing stock to gross domestic product increased by more than 50 per cent from the mid-1990s, peaking at 3.3 times GDP in 2007 and 2010. It has since fallen back to about 2.9 times GDP, similar to that of New Zealand and Britain but much higher than the ratios of the US and Canada. By international standards, this simple measure confirms the view that Australian housing is relatively expensive but by no means head and shoulders above every other country's.

Rising housing debt was the key driver of Australian home prices until 2004 but strongly rising incomes from the commodity boom have played a greater role since.

A reversal of this trend could prompt a severe correction of house prices. A slowing Chinese economy or an increase in global commodity supplies could cause a sharp reduction in incomes and employment.

Monday, March 4, 2013

China's prices down 6% since start of Feb

It's been a China extravaganza in the news lately.

China Gets Tough on Property Sales

China's cabinet, or State Council, said Friday that it plans to enforce a 20 percent capital gains tax on the sale of second-hand homes, as well as higher downpayments and interest rates. Mainland China has tumbled more than six percent since the start of February as government interference with property prices has loomed.

While this has ripple effects — the Australian dollar has weakened — this does not appear to be the start of an economy-wide credit squeeze. Instead, it appears to be limited to the property sector.

60 Minutes Covers the China Real Estate Bubble

Covers the ghost cities. Claims 12 to 24 new cities being built every year. Malls with make-believe brand signs. Multiple classes will be wiped out when the bubble bursts: multigenerational family savings, construction workers. Shanghai average apartment costs 45 times average salary. The fake Manhattan in the port city of Tianjin has ceased development. City officials claim they stopped because they want to put on all the facades at once so they match, but workers say otherwise. First sign of the crash is the migrant workers go home and in this development, at least, they have. Price declines have led to demonstrations outside developers. The head of Vanke worries that a real burst could lead to an Arab Spring situation.

Saturday, March 2, 2013

100 Judges Assigned to Bad Debt Resolution

Wenzhou City Assigns 100 Judges to Resolve Bad Loans, News Says

The judges will work with 50 to 100 financial institutions starting next month to deal with soured assets in the city’s banking system, the state news agency reported yesterday, citing unidentified court officials. Wenzhou’s non-performing loans have soared to 23.86 billion yuan ($3.8 billion), from 8.6 billion yuan in 2011, according to the news agency.That's the trouble with a shadow banking system, it doesn't have a reserve.

The judges will provide legal assistance to companies that have promising outlooks, while weeding out failing enterprises in industries with high pollution and energy consumption through bankruptcy, the news service said.The Chinese are about to learn about the creative destruction portion of the economic cycle.

Tuesday, February 26, 2013

JP Morgan's Fraud Contributed Excessive Credit to the U.S. Bubble

E-Mails Imply JPMorgan Knew Some Mortgage Deals Were Bad

Rather than disclosing the full extent of problems like fraudulent home appraisals and overextended borrowers, the bank adjusted the critical reviews, according to documents filed early Tuesday in federal court in Manhattan. As a result, the mortgages, which JPMorgan bundled into complex securities, appeared healthier, making the deals more appealing to investors.

The trove of internal e-mails and employee interviews, filed as part of a lawsuit by one of the investors in the securities, offers a fresh glimpse into Wall Street’s mortgage machine, which churned out billions of dollars of securities that later imploded. The documents reveal that JPMorgan, as well as two firms the bank acquired during the credit crisis, Washington Mutual and Bear Stearns, flouted quality controls and ignored problems, sometimes hiding them entirely, in a quest for profit.

In an initiative called Project Scarlett, Washington Mutual slashed its due diligence staff by 25 percent as part of an effort to bolster profit. Such steps “tore the heart out” of quality controls, according to a November 2007 e-mail from a Washington Mutual executive. Executives who pushed back endured “harassment” when they tried to “keep our discipline and controls in place,” the e-mail said.

Even when flaws were flagged, JPMorgan and the other firms sometimes overlooked the warnings.

Monday, February 25, 2013

China's Phoenix Island Real Estate Market has Imploded

China’s riskiest property market just collapsed. Is this how it starts?

In some ways (but not all), China is even more exposed to the dangers of a real estate collapse than America was. Washington Post business reporter Jia Lynn Yang pointed out last fall that urban housing stock constituted 41 percent of Chinese household wealth of 2011. The number was 26 percent in the U.S. In other words, Chinese families tend to invest almost twice as much of their money in urban real estate than do American families. So, if you thought Americans were hit hard when that real estate suddenly lost value, it could be even worse for Chinese, who also tend to put much more of their earnings into long-term investments than do Americans. That said, it would also take a bigger drop in prices for the market to collapse, as Chinese buyers tend to put down larger down payments.

And here’s the really scary number: 13 percent of Chinese GDP in 2011 came from real estate investment. 13 percent! If that investment stalls abruptly, as it did in Phoenix Island, the rest of the Chinese economy could follow. That could cause political instability in China and, much more certainly, would set back the global economy.

“As long as the money supply keeps expanding aggressively (15%+ per year), and people (absent alternatives) are willing to plow that money into real estate and hold it, this [real estate market] can persist for some time,” Chovanec explains in an e-mail. “But when the flow of new money slows — either because of the need to rein in inflation, including housing inflation, or the need to roll over and refinance bad debt (often at rising rates of interest) — the whole thing begins to unravel.”More on Phoenix Island Collapse

Chinese manufacturers once snapped up its luxury apartments, but with profits falling as a result of the global downturn many owners need to offload properties urgently and raise cash to repay business loans, estate agents said.

Now apartments on Phoenix Island which reached the dizzying heights of 150,000 yuan per square metre ($2,200 per square foot) in 2010 are on offer for just 70,000 yuan, said Sun Zhe, a local estate agent.

"China had a lending boom... and so if people are using property as a place to stash their cash, they had more cash to stash," said Patrick Chanovec, a professor at Beijing's Tsinghua university.Surprise, it's only worth what someone can pay for it.

"At some point they want to get their money out, then you find out if there are really people who are willing to pay those high prices."

Sunday, February 17, 2013

Current house price correction in Canada has couple more years to run

The correction currently underway will persist for next couple of years.

More adjustment to come in home prices: Carney

“Real wealth is built through innovation, and it’s gained through hard work,” Mr. Carney explained in an interview taped before this weekend’s G20 finance ministers and central bankers meeting in Moscow. “It’s not through some magical asset inflation.”

Mr. Carney said the pace of debt accumulation has slowed to about 3 per cent a year from 10 per cent.

Mr. Carney rejected the suggestion that he may be remembered as Canada’s Alan Greenspan – the former U.S. Federal Reserve Bank chief who many critics blame for inflating the housing bubble in that country – if there’s a housing crash.Sure you will. We look forward to it.

“I’m coming back, so I’ll take responsibility if, if, well, that’s not going to happen,” he said. “I’m also coming back, so I’m here to face the consequences, ultimately.”

Thursday, February 14, 2013

IMF: Canadian Housing 10% overvalued, Currency 5-15% overvalued

IMF warns that Canadian houses are 10% overvalued on average with high variation by area. Also the currency is overvalued.

IMF says Canada housing overvalued, urges more action if needed

Hat tip: vangirl at vancouvercondo.info

The International Monetary Fund, in its annual report on Canada, also said the country's currency was between 5 and 15 percent higher than warranted by long-term economic fundamentals, lifted in part by commodity prices and the country's safe-haven status for investors.

Like Bank of Canada Governor Mark Carney and Finance Minister Jim Flaherty, the IMF worries that highly indebted Canadians make the country more vulnerable to an external shock that could lead to job losses and bankruptcies.

Saturday, February 9, 2013

Toronto Condos Skewing National Data

CMHC Preliminary Housing Start Data Graph of Absorption of Condo units.

The absorption rate has yet to be impacted, and if there are enough wealthy foreigners, perhaps it won't ever be, but the market has yet to be tested. This is quite a bubble of inventory coming in the pipeline, starting to build at around 17 months ago. Assuming 18-22 months is the shortest time from breaking ground to delivery, we have a few more months before people are going to have to get full financing or do a re-assignment, or bail, depending up on their circumstances.

The absorption rate has yet to be impacted, and if there are enough wealthy foreigners, perhaps it won't ever be, but the market has yet to be tested. This is quite a bubble of inventory coming in the pipeline, starting to build at around 17 months ago. Assuming 18-22 months is the shortest time from breaking ground to delivery, we have a few more months before people are going to have to get full financing or do a re-assignment, or bail, depending up on their circumstances.

Friday, February 1, 2013

Netherlands House Prices down 6.3% for 2012

From Statistics Netherlands

House prices more than 6 percent down from twelve months previously

Global Property Guide Netherlands

House prices more than 6 percent down from twelve months previously

Prices of existing owner-occupied dwellings sold in December 2012 were on average 6.3 percent lower than in December 2011. The price drop relative to one year previously is again less substantial than in the preceding month. On average, house prices were 5.9 percent lower in 2012 than in 2011.

Global Property Guide Netherlands

Mortgage market liberalization has also brought new competition. Since 1995, 90% of new mortgages have been not repayable till loan maturity, while 30% do not have to be repaid at all (“interest-only”).

|

| Charts from Global Property Guide |

Monday, January 28, 2013

Canada has about the worst house price bubble in the world

Why Canada has just about the worst house price bubble in the world

Central banks typically raise rates in these situations, the "hard-hearted" approach. But Canada is trying a quieter approach, essential given the high rates of debt.

Canada has a new worthwhile initiative. After years of booming prices, that bastion of politeness north of the border is looking to avoid a catastrophic housing bust for something more, well, boring.

|

| Chart from the Economist |

But by keeping rates where they are and slowly tightening mortgage requirements, Canada hopes to engineer a more gradual price decline that won’t set off a vicious circle. In the best case, prices wouldn’t fall, except below the rate of inflation, so that real prices decline without hitting household net worths. This strategy is hardly unique — China has done the same the past few years — but it has the very Canadian name of “macroprudential regulation.”

Sunday, January 27, 2013

Corrupt Chinese Officials Panic Selling (UPDATED)

But still buying gangbusters in California

The great China corruption fire sale

The threat stated in the above article came from the creation of a property database. Officials Offload Property Original article in the Economic Observer

The great China corruption fire sale

Thousands of Chinese communist officials have been panicked into a fire sale of their illicit properties and billions of pounds have been smuggled overseas as the country's new leaders intensify a campaign to root out corruption.

The CDIC report, which was obtained by the Economic Observer newspaper, suggested that nearly 10,000 luxurious homes had been sold by officials in Guangzhou and Shanghai last year. It also claimed that $US 1 trillion, equivalent to 40 per cent of Britain's annual gross domestic product, had been smuggled out of China illegally in 2012. Economists and experts cast doubt on the figure, but said the flow of money was dramatic. Li Chengyan, a professor at Peking University, suggested that about 10,000 officials had absconded from China with as much as pounds $US100 billion.

The CDIC said 1,100 government officials had fled China during last year's national holidays in October and that 714 had been successful in getting away. In the United States, the National Association of Realtors said properties worth more than $US7 billion had been bought by Chinese in the US last year. Some high-end homes were now built for rich Chinese, with ponds for koi carp and a second kitchen for pungent cooking.UPDATE

The threat stated in the above article came from the creation of a property database. Officials Offload Property Original article in the Economic Observer

According to a university professor who has been helping a city government in Anhui Province set up a home ownership database, officials with a greater degree of political awareness are unwilling to deal with the new property register.

The professor didn't give a clear response when asked why anyone would refuse the simple task of entering data into a computer. Instead, he tactfully noted that "The best solution to the problem is to pass the work on to a university, get them to submit a report, and, once funds have been allocated, find some students to do the work. In this way, both research and work can be done, and they won't have to worry about the risk of leaking information."

A person in charge of a real estate agency told the Economic Observer that since November last year, the instances of officials hurriedly offloading their properties had increased around the country, and these properties are often luxury residences, sometimes worth more than 10 million yuan if they're located in first-tier cities.Hat tip: UBC in Crisis Mode commenting at Vancouvercondo.info

Only a portion of these houses are being sold through real estate agents.

Some property owners prefer to let state-owned institutions or even professional agents handle the sale. In this way, they won't need to expose themselves during any part of the process.

According to statistics posted on the website of the Beijing Municipal Commission of Housing and Urban-Rural Development, 7,940 contracts for second-hand housing deals had been signed in the first half of January 2013, an increase of 360 percent over the number of transactions completed in the capital over the same period last year.

Monday, January 21, 2013

Hong Kong most unaffordable English-speaking, Vancouver second

Demographia's 2013 survey is out.

Demographia 2013 International Housing Affordability Survey

All numbers are median multiple, which is the median house price divided by the median income for the given geography.

All numbers are median multiple, which is the median house price divided by the median income for the given geography.

Hong Kong 13.5

Vancouver 9.5 (and improvement from 10.6 last year)

Sydney 8.3

San Jose 7.9

San Francisco 7.8

London 7.8

Melbourne 7.5

Adelaide 6.5

Perth 5.9

Toronto 5.9 (a surge from 5.1 last year)

Brisbane 5.8

California appears to be re-inflating the bubble. If interest rates aren't normalized soon, the U.S. is going to repeat the cycle already. 20 major markets were ranked as affordable down from 24 last year.

Demographia is pretty single minded about what causes housing in-affordability. For example, in the report Honolulu and London are mentioned as being severely unaffordable, no reason is given why this might be true in Honolulu, but London's dear market is caused solely by restrictive land use policies. The report doesn't mention what any local could tell you: outside money is pouring into both markets. Basically, capital inflows is not discussed in these reports and cheap credit given only a nod.

Somehow (not explained why) these policies had negligible effect on prices for a decade and a half. Then, suddenly, oddly enough, when financial markets were deregulated at the end of the 1990s and into 2000s, the end result of which cheap mortgages were being pushed at anyone and everyone, then prices soared into unaffordable range.

Somehow (not explained why) these policies had negligible effect on prices for a decade and a half. Then, suddenly, oddly enough, when financial markets were deregulated at the end of the 1990s and into 2000s, the end result of which cheap mortgages were being pushed at anyone and everyone, then prices soared into unaffordable range.

Land use policy is a symptom. Municipalities engage in it to reduce externalities and improve quality of life. Something Demographia doesn't want to grasp. I get the sense reading their reports that they resent that developers cannot always socialize so much of their costs. Or I guess they dream that if people could just build at will on the side of old spatter cones, and in tsunami inundation zones, Honolulu's high prices would just magically vanish.

Hong Kong 13.5

Vancouver 9.5 (and improvement from 10.6 last year)

Sydney 8.3

San Jose 7.9

San Francisco 7.8

London 7.8

Melbourne 7.5

Adelaide 6.5

Perth 5.9

Toronto 5.9 (a surge from 5.1 last year)

Brisbane 5.8

California appears to be re-inflating the bubble. If interest rates aren't normalized soon, the U.S. is going to repeat the cycle already. 20 major markets were ranked as affordable down from 24 last year.

Demographia is pretty single minded about what causes housing in-affordability. For example, in the report Honolulu and London are mentioned as being severely unaffordable, no reason is given why this might be true in Honolulu, but London's dear market is caused solely by restrictive land use policies. The report doesn't mention what any local could tell you: outside money is pouring into both markets. Basically, capital inflows is not discussed in these reports and cheap credit given only a nod.

Each of Australia's major markets, with the exception of Sydney had housing affordability within the 3.0 Median Multiple norm during the 1980s, before the widespread adoption of urban containment policies, which is referred to as "urban consolidation" in Australia.

Land use policy is a symptom. Municipalities engage in it to reduce externalities and improve quality of life. Something Demographia doesn't want to grasp. I get the sense reading their reports that they resent that developers cannot always socialize so much of their costs. Or I guess they dream that if people could just build at will on the side of old spatter cones, and in tsunami inundation zones, Honolulu's high prices would just magically vanish.

Wednesday, January 9, 2013

Royal LePage admits Vancouver prices vulnerable

BMO economist says prices in Vancouver could fall a further 5% in 2013

Royal LePage would only cop to a 3% decline due to weakness in the luxury market. (By the way, your average prices should be the luxury market, one sign of structural issues in said market.)

Vancouver house prices to decline further, real estate panel predicts (updated)

Ottawa all prices were up 1.22% and residential class were up .6%

Toronto all prices all TREB were up 6%, detached up 6.2%, Toronto detached up 2.9%.

Vancouver is up 1.3% on average according to yattermatters.com's numbers.

I don't think Royal LePage imagined how lofty Toronto could get. Median prices in Toronto are down 6-14% since April, depending upon area/type.

Vancouver's average is down 14% since February, which show you how volatile averages can be. February's numbers will be a better comparison to last February. Vancouver's prices have not shown a strong annual cyclic behavior (sales and inventory have, but not prices).

Royal LePage would only cop to a 3% decline due to weakness in the luxury market. (By the way, your average prices should be the luxury market, one sign of structural issues in said market.)

Vancouver house prices to decline further, real estate panel predicts (updated)

Housing prices are about 10 times average family incomes, Guatieri said, putting "Vancouver in the upper echelon of overvalued housing markets, not just in Canada, but across the world."But only a five percent drop off that? Over twelve months? Does he have a mandate to prevent panic?

"There is some speculation that wealthier foreign buyers are waiting to see if the government will restart that program before they purchase a house in Vancouver," Guatieri said. "What has supported Vancouver's housing market, at least in the past five years, is not income, it's wealth. A lot of that is foreign wealth, although we can't quantify that."Which brings us to the Suitcases full of Cash article on Yahoo Suitcases of Chinese cash flooding Canada’s borders (Hat Tip Anonymous commenting at Vancouvercondo.info)

Nearly $13 million in cash was seized during that period, the newspaper reported, citing Canada Border Services Agency data obtained under the country's access to information legislation. Most of the money was returned. In one case at Vancouver's airport, a Chinese man was found with $177,500 in the lining of his suitcase and stuffed into his wallet and pockets. He was fined. The financial penalty was roughly $2,500, a relatively small price to pay for evading strict foreign-capital controls imposed by Beijing.Back to the Sun article:

Royal LePage forecasts that fewer high-end sales will cause average prices in Vancouver to drop three per cent by the end of 2013. Nationally, Royal LePage forecasts a one-per-cent gain in the average home price by the end of the year.Let's look back at what Royal LePage predicted for 2012, shall we? Royal LePage Predicts Further Home Price Appreciation Contrary to Recent Talk of Decline

Royal LePage expects average price growth to continue through 2012 and predicts national average prices to increase by 2.8 per cent by the end of the year.Let's see how they did. December to December 2011 to 2012

. . .

At the end of 2012, average house prices in Ottawa are forecast to be 3.3 per cent higher than 2011.

. . .

At the end of 2012, average house prices in Toronto are forecast to increase 2.6 per cent over 2011

. . .

At the end of 2012, average house prices in Vancouver are forecast to be 2.3 per cent higher than 2011.

Ottawa all prices were up 1.22% and residential class were up .6%

Toronto all prices all TREB were up 6%, detached up 6.2%, Toronto detached up 2.9%.

Vancouver is up 1.3% on average according to yattermatters.com's numbers.

I don't think Royal LePage imagined how lofty Toronto could get. Median prices in Toronto are down 6-14% since April, depending upon area/type.

Vancouver's average is down 14% since February, which show you how volatile averages can be. February's numbers will be a better comparison to last February. Vancouver's prices have not shown a strong annual cyclic behavior (sales and inventory have, but not prices).

Friday, January 4, 2013

City of Toronto Detached Prices Down $94,000

According to TREB Market Watch Median house prices in the City of Toronto have fallen $94,000 since their peak in April 2012. The median price then was $656,000 and this December 2012 it has fallen to $562,000.

Thursday, January 3, 2013

U.S. GDP per capita is significantly higher, why are house prices lower?

Global MetroMonitor Interactive Graph from the Brookings Institute

A chart of "real GDP per capita and employment change for the largest 300 metropolitan economies"

As a little thought experiment, do a cross-border comparison of GDP per capita between the U.S. and Canada. Seattle: 65k, Vancouver: 41k. Or more startling Toronto: 43k, Buffalo: 58k.

As a little thought experiment, do a cross-border comparison of GDP per capita between the U.S. and Canada. Seattle: 65k, Vancouver: 41k. Or more startling Toronto: 43k, Buffalo: 58k.

Where in the world is the wealth generation supposedly coming from to justify double the house price in Canada?

A chart of "real GDP per capita and employment change for the largest 300 metropolitan economies"

Where in the world is the wealth generation supposedly coming from to justify double the house price in Canada?

Wednesday, January 2, 2013

China banks unprepared for interest rate liberalization

Bank profits fading as interest rate reform begins

At the same time Japan's new PM Abe has made noise about raising the target inflation rate there. What's moving Japanese markets?

About 52 percent of surveyed bankers said that interest rate liberalization should take place in the period from 2015 to 2017, while only 2.8 percent of the bankers agreed that 2012 is the right time, the report showed.Real banking reform would impact the economy broadly, the copper "carry trade" would be put out of business, all the way up to the savers' subsidizing of state and well-connected industry. Whether banks will shift to providing funding to SMEs as hoped isn't clear. Default rates are high and it seems unlikely banks will allow rolling of principal and back interest into a new loan as they do for project funding.

The result indicates most of the bankers were not prepared when the central bank made the first move toward a more market-driven rate by doing away with a universal fixed deposit benchmark interest rate. The central bank lowered the benchmark on June 7, and allowed rates to fluctuate up to 10 percent above the benchmark for commercial banks.

At the same time Japan's new PM Abe has made noise about raising the target inflation rate there. What's moving Japanese markets?

In my opinion, a higher inflation target by the Bank of Japan is not particularly interesting. After all, the Bank of Japan can't hit the current "goal" of 1 percent inflation. I don't have much faith that renaming the "goal" a "target" and increasing it to 2 percent will be like waving a magic wand. But something much more significant is afoot - the possibility of explicit cooperation, albeit perhaps forced cooperation, between fiscal and monetary authorities. The loss of the Bank of Japan's independence to force the direct monetization of deficit spending is the real story.

Subscribe to:

Posts (Atom)