Waiting to get into the market can be a frustrating adventure. You weathered the mass hysteria and now everyone who thought you were an idiot is avoiding you at parties because they are afraid you are going to say "I told you so." (Believe me, many will claim they also saw it all along. Get used to it.)

Buying is 99.9% about emotion. Bolster that .1% of logic to make it as strong as possible. You are your own worst enemy.

When housing prices fall the economy enters a deflationary period. This is not a condition you are used to. Interest rates remain rock bottom, but cash is king. How much sense does that make?

Decide on your entry point. This will bring sanity back to your life. To pick an entry point, first decide what kind of recovery you think the market is going to have.

- Given global economic conditions and long-term emergency interest rates which can barely get lower, do you think government stimulus is going to bring housing back all at once? How likely are additional round of first time buyer stimulus checks that juice the market just a little longer?

- Do demographics increase demand ongoing or decrease it? (Will a large influx of young buyers will appear relative to retirees?)

- Is the immigrant policy going to change? (Note: most immigrants are poorer than the average Canada-born citizen, Rich home buyers get all the press, but they are not the norm.)

- What do you expect Canadian five year bond rates will do? (This determines how much total mortgage debt is allowed to grow. No growth == price declines no matter what else is happening. Low rates means credit will not be weighing on prices.)

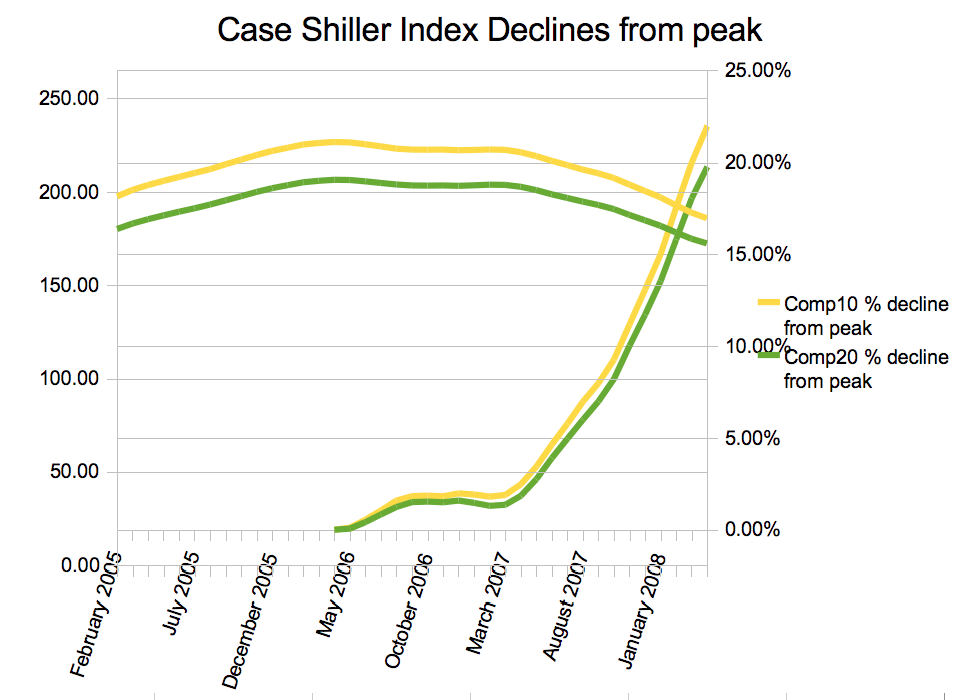

If you expect a V shaped recovery, then you need to be ready to jump. Get your financial house in order so you qualify for the best mortgage possible. If not, you can take your time and shop relaxed and save save save. The U.S. market is six years ahead of Canada and makes for a possible price model. (A pretty good one, I think, but this is your call.)

Familiarize yourself with past bubbles as fortification for your emotions. Here is a classic asset bubble price chart, along with the dominant emotion in the market.

Here is a link to an interactive chart of some major bubbles since 1976:

http://www.macrotrends.org/1311/asset-bubbles-since-1976 You may feel alone, but you are just the latest participant in a centuries old grand tradition of economic cycles. Nothing has changed, and barring some significant wisdom on the part of policymakers, it never will. So cheer up. This is just the way it is. Those who ignore history, etc etc...

Things to consider when choosing a property in a down market:

Do not buy from someone who bought near the top. They didn't have any money for maintenance. Keep an eye on past sale dates before you fall in love. Hidden damage from poor maintenance will cost you more than a lower price.

You will have your choice of properties, but don't buy in the middle of quality if this is your first home. Spend more for something in great shape with no overwhelming maintenance issues, or spend low for something in need of repairs where you have lots of cash left to make them. Don't buy in between. It's the worst of both worlds. If you are thinking of the house as a canvas for expressing yourself, no reason to pay the premium for quality you are going to rip out. Contrarily, if you are buying because your family is expanding and you will not have time or energy, spend the extra up front for something you can neglect for a decade.

First home buyers who plan to move up. PLAN TO MOVE UP. Don't buy everything you would ever want in a house in your first house. It will break you. Like your first car as a teen, buy a house that is cheap to repair (simple rooflines, well landscaped for drainage) rather than one that makes you feel good about yourself. This is shelter, first and foremost. You can still overspend in a down market by moving upmarket because you keep thinking you can get so much more for just a bit more money. Don't get stupid now of all times after you were so smart earlier.

If you may be exiting the property while the Boomers are still buying, buy a retiree friendly house. This submarket will do better over the medium-long term. That would be a house that can be lived in strictly on the ground floor. Wide hallways and bathrooms that a walker can navigate. And a host of other features you will want to research before purchasing. If you must buy before you feel it's the bottom, buying in this segment will help the house hold value.

Other thoughts

Once automatic annual gains are gone, you should switch to a mode of preserving capital. Until prices absolutely bottom, real estate will not even function as a hedge against inflation. Do the calculations for your situation.

Rent vs. Buy calculator (under revision at the mo) or

this one in the interim. Remember as you examine all the scenarios that you are preserving wealth by exchanging renting property for renting money. Always remember you are leveraging when you buy. Something you almost never do and as a result do not instinctively take account of the outsized downsides. (A 100% price gain is wiped out by a 50% price decline without leverage. A 20% downpayment is wiped to zero by a 17% decline with leverage.)

Your downpayment is not the price of admission. Its loss has real impact as missed investment capital. Imagine you hate the house you are thinking of buying and calculate this purchase to death before pulling the trigger. If prices fall another 15%, where will you be financially vs. where you would have been without buying.

Put less down and keep some cash for emergencies. At least 10k. Houses can bite you overnight. Do not become cash poor just because you bought a house. It will not increase your quality of life.