Hong Kong Stocks Fall as Wen Says China Will Keep Property Curbs

Industrial & Commercial Bank of China Ltd. slumped 1.6 percent after Premier Wen Jiabao said China will “firmly” maintain restrictions on the real-estate market.

Industrial & Commercial Bank of China Ltd. slumped 1.6 percent after Premier Wen Jiabao said China will “firmly” maintain restrictions on the real-estate market.

Despite representing only 25 per cent of Australia's population and 38 per cent of households, the baby boomers collectively hold 49 per cent of Australia's housing assets.

The baby boomers collectively own 46 per cent of owner-occupied housing assets, 7 per cent of which is made up of housing debt. In comparison, the baby boomers hold 57 per cent of "other" dwellings, 14 per cent of which comprises housing debt.

In fact, a recent survey of people aged over 60 found that 22 per cent are "very likely" and a further 10 per cent "likely" to sell their homes and buy a smaller property to fund their retirements. By contrast, there was very little support for the third and fourth options above, selling and renting or taking out a reverse mortgage.

According to Australian Taxation Office (ATO) data, 78 per cent of property investors are lower-to-middle income earners (i.e. they earn less than $80,000 a year) and three-quarters of these investors are negatively geared - i.e. losing money and investing purely for capital gain.

There is, therefore, the risk that the baby boomers will soon switch from net buyers to net sellers of investment properties due to the low yields on offer (about 3 per cent after costs) and, in the case of boomers who are negatively geared, the inability to claim tax deductions against other income once they cease working.

A group of around 400 homeowners in Shanghai demonstrated publicly and damaged a showroom operated by their property developer after the company said it cut prices. Home buyers had wanted to speak with the developer to refund or cancel their contracts but were unsuccessful, according to local media. One report said the price cuts exceeded 25% per square meter.Sentiment online was not supportive of the protesters.

“This is an immoral action,” Weibo user Xiaobai Yeyou Naxieshi wrote in one of the 7 million property-related posts Sina had collected Tuesday on a special topic page. “Buying a house is a form of investment and every investment involves risk. If prices didn’t fall, people who can’t afford to buy an apartment would really have to wait forever.”

“Dear Government, can you please cancel my purchase of Petrochina shares? A refund based on the IPO price would be fine,” joked Linshi Renyuan. Petrochina, which debuted on the Shanghai stock market at 16.7 yuan per share in 2007, was trading at to 9.85 yuan per share at the end of the day Tuesday.

House prices in Australia have been growing steadily now for the past 15 years, but the income of everyday Australians has not kept up.So, where exactly does the money come from to drive the price of houses? Look ma, it's not wealth, it's debt!

Figures from RP Data show the average Australian income is now between $55,000 and $60,000, but a typical house is worth around $450,000.Ouch.

With the cost of living included, this means the median dwelling price is around 6.5 times disposable income for households, more than double what is considered affordable.

"I think the most likely scenario is small house price declines, similar to what we've had in the last 12 months, so where prices are sort of probably down 3 to 5 per cent," [Macquarie Group senior economist Brian Redican] said.Spoken with authority.

Many people were engaged in speculative real estate investments a few years ago, according to Ms. Song, an Ordos resident. But recently almost half of Ordos’ real estate businesses have closed or are facing closure, a real estate agent told The Epoch Times.

“Many real estate companies in Ordos have been facing disruption of their capital chain, which will get worst by the end of the year,” financial analyst Li Huizhong, who investigated private capital in Ordos, told China’s National Business Daily.

More than 80 percent of property development in Ordos has been financed by private lending, according to the report [from the Ministry of Housing and Urban-Rural Development].

A lot of money from private lenders has also gone into the real estate market, Zhou Dewen, chairman of Wenzhou's Small and Medium Enterprise Development and Promotion (SMEDP) told Zheshang Magazine. Only 35 percent was invested in businesses, according to a report by the Central Bank’s branch in Wenzhou.

Su Yelu is the latest property developer to be detained by public security officials after allegedly fleeing last month with a large amount of unpaid debts. Two years ago, Su was only a restaurant boss in the downtown area in Ordos. Ambitious to build a hotel, she borrowed money through her workers and their families, who hoped to earn high interest, according to some mainland media.

As the property sector in Ordos tightened when Beijing acted to cool the property market, Su's business failed, her hotel not finished. Her case is said to have involved 4,000 creditors.

The temporary profitability of informal banking seems to have also lured many SOEs to participate in the business, sometimes on-lending funds borrowed from banks to earn high spreads. Even listed companies got into the game, including Singapore-listed Yangzijiang Shipbuilding; it was reported that more than 25 per cent of the company's pre-tax profits in the second quarter came from its loan activities.

According to Japan-based Nomura Securities, the size of China's shadow financing could amount to 8.5 trillion yuan ($1.33 trillion). Liu Jigang, a researcher from ANZ bank, estimates it could even be as high as 10 trillion yuan. These estimates may not be accurate, but they nonetheless highlight the problem of shadow banking in China.

None-bank loans were only 8.7 percent of the total yuan loans in 2002, but had grown to 79.7 percent in 2010. This growth in finance means the loan size is no longer an index of money supply-demand relations.

The high returns attract more economic participants and even State-owned enterprises (SOEs) have joined the game. According to the Financial Times, several jumbo SOEs have financial platforms, while 90 percent of all loan-lending enterprises are SOEs.This last one is interesting as it is written by a researcher at the State Information Center. The usual pattern of articles with any dire economic tone is to follow the bad news with a policy section. I always assumed the bad news was a kind of semi-official red flag to warn the reader that the central government is serious about the policy in question. This article contains no policy announcement.

And the calls seem to be getting more outlandish, with the latest prediction being for a 20 per cent drop in Australian house prices between now and the end of 2013.A whole 20%! That would be a 24% fall overall since the peak (approximately). Again for future reference.

It is the long-term trends in underlying demand and supply that drive housing prices.No, it's access to credit that drives prices up. If tomorrow, everyone were forced to pay with cash only, what would the price of houses be? (Yeah, I know, kinda makes your brain stop imagining that, doesn't it?)

Increases in the ratio prior to 2003 were due in large part to structural changes in the economy which increased the availability of housing credit.Whoa there, Kemo Sabe. You admit that access to credit drove the bubble before 2003, but somehow, not after that? And that there was no correction for the pre 2003 bubble, either?

More importantly, Australian households remain highly able to service their housing debt, with arrears still at low levels when compared internationally.Yeah, if you cherry pick the numbers. Sure. I notice you failed to mention that Australian household debt levels are recordbreaking (north of 154% of income, compared to 118% in the late 90s early 2000s), especially compared internationally. You and Canada are really duking it out for worst debt-ridden. Both in excess of the U.S. at our most, um, excessive.

And China’s demand for iron ore has not been on a stable upwards trend but rather it has been growing exponentially. Basically, the amount of iron ore the country sucks in has been doubling every three years. The investment in Australia’s largest resource projects to help meet this and other demand is in the main locked in. In other words, no matter what happens in Europe, we have roughly a two-year period where business investment will contribute strongly to our growth.Hey, China is going to buy enough over-priced iron ore to bail out the economy. Iron ore, really? Australia loves being an economic colony, apparently. Export raw materials, import finished products. . . And by the way, it's 5.6% of total GDP and less than 1% of your national workforce, mining is. But it is going to help all those masses of Aussies get out from under their recordbreaking debt burden. Yeah, you've definitely proven your point there.

Using fiscal and monetary policy to stimulate the economy when needed is entirely appropriate and the prospect should not be ignored when expressing a future outlook.Ha. And if all else fails, we'll kick the can down the road. Oh, I'm totally convinced.

Justification as to why the crash didn’t happen has subsequently been far from convincing.Kinda like this article you just wrote, you mean?

In economic terms the claim can be shot down on both theoretical and empirical grounds, but there is a risk that doing so gives more oxygen to such a claim when instead it should be doused.You started drinking before you finished writing. And you were doing so well too.

Everybody is entitled to their opinion, but individuals should refrain from frightening people with opinions that by their very nature generate scary headlines, but that fail to transpire.And cheerleading a bubble so even more young people are sucked into debt slavery isn't irresponsible?

"It must be something political or social because it certainly has nothing to do with economics." [Ward McAllister, president of Ledingham McAllister Properties] said.

He forecast low-interest rates for the foreseeable future, which will translate into continuing sales.

"There is no bubble in Vancouver," [Richard Wozny, of Site Economics Ltd.] said.

McAllister had advice for prospective homeowners in their 20s who are questioning whether they should wait for prices to come down: Don't wait, borrow from mom and dad. And he warned against selling, hoping to get back into the market later.

"Affordability is one of the main concerns in this market and I think will continue to be over the rest of my life."

This occurs a few times every decade but it seems to suffering overuse since the global financial crisis in 2008.Were you sober when you wrote this?

But what is the average Aussie home? Who knows? That is exactly why these wild generic statements are rarely accurate.Now you are just jerking us around, right? "Wild generic"?

But are we really about to suffer massive house deflation?This is a bold statement going into the big spring season, my friend. Steady is not actually what you want to see at this time if you are a bubble cheerleader.

It is very unlikely. And it's unlikely because in many places deflation has already occurred and values have steadied.

Prices have steadied, and dropped in some markets, it is true, but there is always an upside to a decreasing market and that is of course that it is great for buyers.Actually, as you are going to see, soon enough, it's not great for buyers. It's a trap.

My advice is don't panic. Get to know the market you want to buy in, I mean really get to know it, study sale prices over the last decade, buy in areas where you can secure a good deal and do not over-commit on your mortgage.The last decade encompasses the credit bubble. That sounds like a horrible idea. And, of course, don't over commit on the mortgage. Warnings like this have a built-in assumption that the bank will happily allow you to do exactly that. I'd call that a red flag.

Well, if your home is listed with a price expectation of 10 per cent more than it is really worth, add a further 5 per cent and yes, you could see yourself "lose'' 15 per cent.What? I've read that three times and I have no idea what it means. Maybe because I haven't drunk as much as you have yet tonight. "Average" and "really worth" are equally meaningless, by the way. Also "true realistic"?

But how much of a true realistic value is that?

The heavy losses being faced in the UK and US were caused by bad lending practices and housing policies that just don't exist in Australia. They stretched residents in those countries well beyond their means and created a property bubble. But even in these depressed markets, there are signs of recovery.No, they were caused by a credit bubble, which you definitely have. As well, your residents are deeply stretched, and no there isn't much of a recovery, unless you are cherry picking some "average" of your own in areas where Australians, Canadians and others are buying up property. To return to the long-term average burden for a household, housing in the U.S. needs to fall farther yet.

Using data from the Household, Income and Labor Dynamics in Australia survey, Professor Wood tracked the housing histories of thousands of Australians over nine years. During that time 1.65 million ''episodes'' of home ownership were terminated as people moved into rental housing. Among people under 50, the ''survival rate'' in home ownership was 77 per cent.

The former owners who did not return quickly to the property market were more likely to enter public housing or qualify for Commonwealth rent assistance than long-term renters.In other words, owning a house nearly bankrupted these families.

Economists are predicting a double-edge sword for Sydney's property market, forecasting the median price to boom from $644,000 to $770,000 in the next three years - on the back of the housing crisis.

The report, prepared by BIS Shrapnel, says the underlying strength of the Australian economy, stable interest rates in the short term, high immigration and a dire shortage of houses in Sydney, will be the main drivers of this growth.

It forecasts the Sydney median house will lift by 19 per cent to $770,000 over the three years to June 2014.

This compares with 20 per cent in Perth, 16 per cent in Brisbane, 8 per cent in Canberra and only 6 per cent in Melbourne.

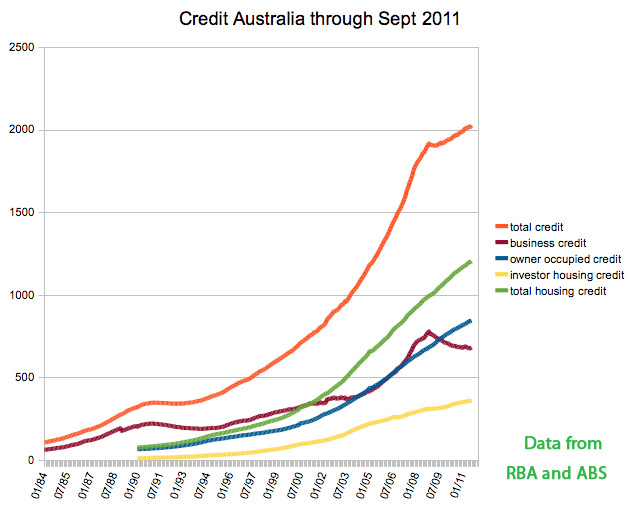

|

| Total housing credit issued in Australia through Sept 2011 |

|

| Credit issued in Australia through Sept 2011 for business and real estate |

| BIS Shrapnel predictions, tan line Oct 2009, blue line Oct 2010 |

Such illegal lending amounts to about $630 billion a year, or the equivalent of about 10 percent of China’s gross domestic product, according to estimates by the investment bank UBS.

Already, according to a recent survey by the city’s small-business council, one in five of Wenzhou’s 360,000 small and medium-size businesses have recently stopped operating because of cash shortages.

Shanghai, for instance, experienced the worst Gold Week holiday in 6 years. Only 398 units were sold in the primary market for the entire the 7-day long holiday, which is only 20% of the same period of last year (in other words, sales dropped 80% year-on-year) according to cnyes.com. According to Xinhua, one developer in Jinan tried to sell their flats by offering gifts like iPads and other electronic products, but without much success. Beijing has been doing somewhat better according cnyes.com, as 866 units were sold in the first 6 days of Golden Week, only 10% fewer than last year, but 62% lower compared to the first week of September. In Nanjing, one developer even offered a buy one (house) get one (flat) free (BOGOF) according to Xinhua, as that developer has failed to sell those houses since December of last year.

Any move by Beijing to institute new regulations to limit this activity may prove to arrive too late. Speculative tools like copper and real estate have been used in informal and formal lending, making them harder to regulate, thus increasing China’s vulnerability to price declines and financial risk. Beijing understands it needs to clamp down on copper speculation, but it is wary as this may lead to a big rise in non-performing loans at banks.

[I]t was reported that several business executives in Xiamen in neighboring Fujian province have also gone on the run because they could not pay back money borrowed from loan sharks.

Local police reported that about 12 billion yuan (US$1.88 billion) is involved in cases of fugitive bosses, according to Strait Herald in Xiamen.

According to an insider of the private lending market in Xiamen, although government authorities have not published information, reliable resources say local police have received reports of loan shark cases involving amounts of up to 12 billion yuan (US$1.88 billion).

The report indicated that 60-70 creditors were directly involved in these cases and represented about 600-700 smaller creditors in turn.

Total deposit outflow from regular banks to the private lending market has been around 3 trillion yuan (US$470.37 billion) during the first three quarters of this year, according to Liu Mingkang from China’s Banking Regulatory Commission.

Sixty-four listed, non-financial companies, 90 percent of which are state-owned enterprises, have invested 16.9 billion yuan (US$2.65 billion) in private loan lending.

In Ordos, Inner Mongolia, 50 percent of residents are involved in underground lending, whereas in Wenzhou, 89 percent of families and 60 percent of businesses are engaged in similar activities.

Ms. Li, who works for a foreign company in Shanghai, told The Epoch Times that her parents have deposited about one million yuan (US$156,800)--their entire life savings and money they made from selling a house--into a small private lending company in Wenzhou, at a 2 percent monthly interest rate. This investment brings them an additional monthly income of 20,000 yuan (US$3,000).

The deal was so sweet that her parents then applied for a secured loan of 800,000 yuan (US$125,000) from a regular bank on another house they owned, and invested the money with the same private lender to earn extra cash, Li said.

Like Li's parents, many ordinary Chinese have been pouring money, including their life savings, into the underground lending market.

|

| Chart of monthly sales of single family homes SFH in Vancouver over five years |

|

| Chart of Prices of Detached and All Sales in Vancouver 2010 2011 |

|

| Year on Year change in house prices Vancouver |

|

| Year on Year change in house prices by Vancouver region, smoothed over 4 months. |

The private-loans market in Wenzhou has created a network of underground financing that is thought to have drawn in nearly 90 per cent of households and 60 per cent of local companies.Talk about far reaching impact on the citizenry of China. Imagine if Bernie Madoff had sucked in the savings of 90% of New Yorkers.

The chief concern, one that evidently has begun to trouble Beijing, is that the underground lending networks are so pervasive that each default is wildly magnified. A collapse in the loan triangles between companies, shadow banks and private investors seems inevitable.

Australian Tax Office statistics from 2008-09, analysed by AAH, showed that after landlords took in $24 billion in rental income, they claimed $30 billion in losses, allowing them to write off about $6.5 billion in taxes.

China's State Council announced this weekend that local governments that have failed to complete the construction of planned subsidized housing projects will not be allowed to construct or buy new official buildings.

Of the subsidized-housing projects that the government plans to have built in 2011, 86 percent were under construction within the first eight months of the year, according to statistics from the Ministry of Housing and Urban-Rural Development.One does wonder what constitutes "under construction". Girders being ordered? A single shovel in the ground?