The former librarians were shocked to discover that for about half the price, $295,000, they could get everything they’d hoped to find in Toronto — a cool condo close to a burgeoning arts scene, thriving cafes, up-and-coming restaurants, and bike paths that meander along a waterfront undergoing a rebirth.

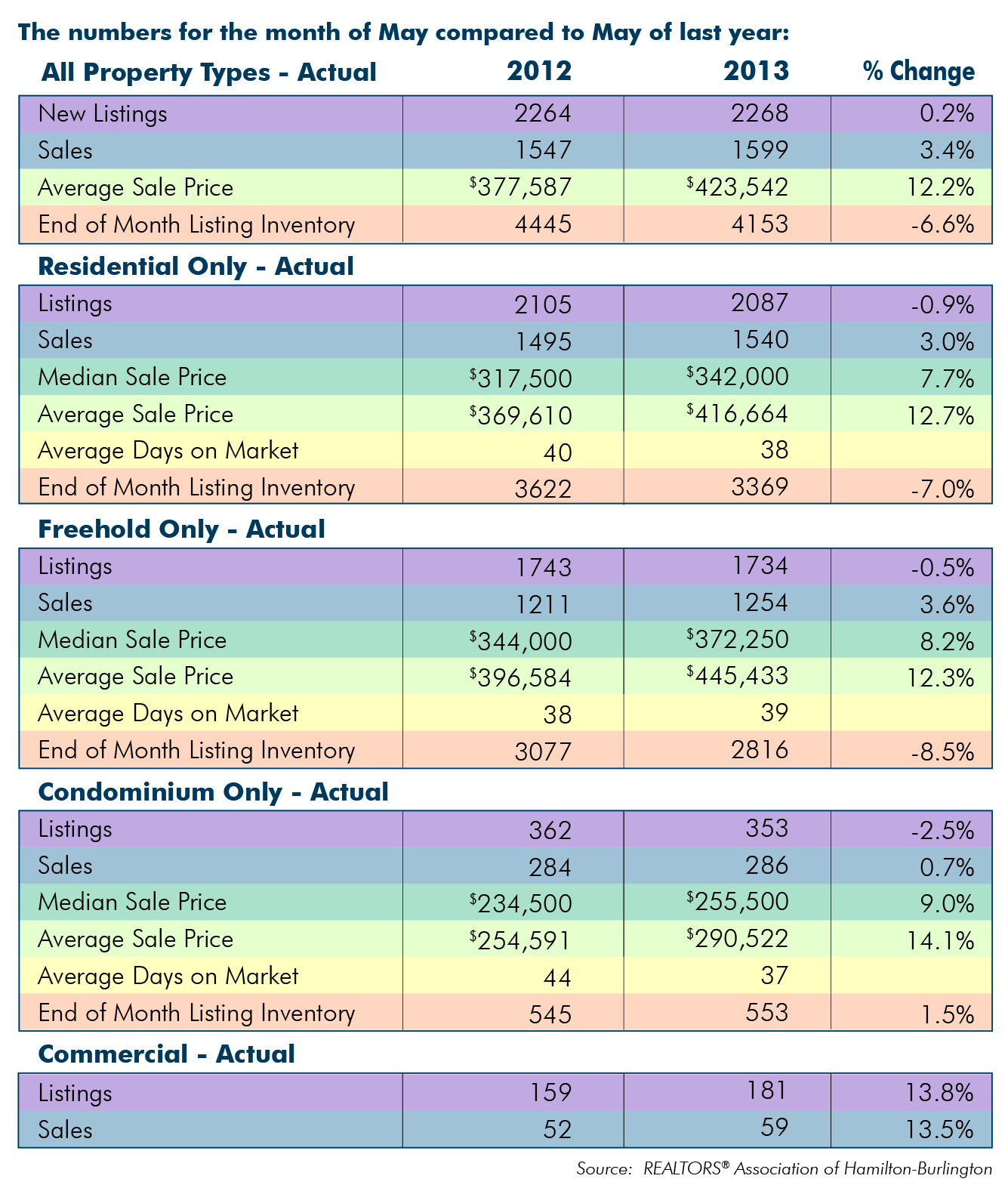

There they discovered elegant, and sometimes unloved, brick Victorians, charming workers’ cottages and even Rosedale-like mansions. And they were all shockingly affordable — at least by Toronto’s sky-high standards.Median price for residential was $342,000 last month according to the RAHB chart for May 2013

{kind=link}

Median household income was $79300 using statcan.gc.ca and applying the last 4 years average median increase to the latest data.

Resulting in a median multiple of 4.3x.

Not sustainable, but more interesting in the medium term is what will the fallout be. As Toronto wanes will Hamilton continue to be seen as a boom town and weather the national downturn better, or will a contraction hit harder due to the weaker base to fall back on. If it remains clear that the transport project will finish I expect more of the former.